Should we buy?

March 11, 2008 11:20 AM Subscribe

Buying a house during a boom. Wife says right away. I say wait. Help convince us either way.

We are buying to live not to speculate. Both financially secure. Have a good size down payment.

Because of the commodity boom? housing prices here (Vancouver) have, (in my opinion) gone nuts, increasing about 10% a year for the past decade. I don't know if this is a bubble or not...

Anyways, I say that if prices can go up this fast it's possible that they can go down a lot too; hence we should rent a bit longer. She says we're wasting our money renting.

I figure that even a 10% downturn would save us $30-50k: several years rent.

Am I wrong? Is a correction like this unlikely? Am I thinking too much about Money and not enough about a Home?

We are buying to live not to speculate. Both financially secure. Have a good size down payment.

Because of the commodity boom? housing prices here (Vancouver) have, (in my opinion) gone nuts, increasing about 10% a year for the past decade. I don't know if this is a bubble or not...

Anyways, I say that if prices can go up this fast it's possible that they can go down a lot too; hence we should rent a bit longer. She says we're wasting our money renting.

I figure that even a 10% downturn would save us $30-50k: several years rent.

Am I wrong? Is a correction like this unlikely? Am I thinking too much about Money and not enough about a Home?

Have you calculated the cost of renting versus the cost of owning? How much do you pay in rent and how much would you pay in interest, insurance, taxes, maintenance, repairs, gas, electricity, etc? That would be the most important comparison. You should also consider the non-economic costs an benefits of buying a house versus renting if there are any difference (e.g. increased hassle to deal with repairs, a longer commute, more space, positive feelings of ownership, and so on). This will answer the question of whether or not you are wasting money renting.

I don't think anyone here can tell you what the future will hold for the Vancouver real estate market (though people can speculate and maybe make somewhat educated guesses), so your best bet is to figure out how a house purchase will affect your cash flow.

posted by ssg at 11:39 AM on March 11, 2008

I don't think anyone here can tell you what the future will hold for the Vancouver real estate market (though people can speculate and maybe make somewhat educated guesses), so your best bet is to figure out how a house purchase will affect your cash flow.

posted by ssg at 11:39 AM on March 11, 2008

Here is a Buy vs. Rent calculator that I've found to be helpful. It allows you to plug in expected appreciation (and despite the warning, it does allow you to plug in negative appreciation if that's where you think your market is heading,) and a number of other factors.

posted by EmptyK at 11:44 AM on March 11, 2008

posted by EmptyK at 11:44 AM on March 11, 2008

I feel that it is generally better to buy if you can afford the downpayment. Once you're in the game you keep up with the increases in the cost of housing and over time the true cost of your mortgage payments is eaten away by inflation; you're unlikely to be paying the same rent in 25 years whereas your mortgage payments will only change based on interest rate changes which could go either way. My mortgage payments went down the last time my mortgage came up for renewal - this never happened to me when I rented.

As an example I have several neighbours who live in houses worth over $700K in Toronto who probably pay a fraction of what I pay - I would guess in the neighbourhood of $900 monthly - because they have lived there a long time. Based on their income alone it would literally be impossible for them to buy the house they currently live in. Or, as one California real estate blog put it: how can you afford to live in Palo Alto when you only make $125K? Buy the house in 1992.

Housing prices have increase much faster than earning or the cost of living in general so it's become relatively harder to buy a home. Some would say that this calls for a correction. I do not believe this to be the case - in places like Vancouver it's a simple case of supply and demand. Demand for Vancouver homes has outstripped supply and will continue to do so into the foreseeable future. This, IMO, leads me to conclude that even if the Vancouver economy went into the shitter house prices would remain high until things got so bad that there was a mass exodus out of the city. Vancouver is a long way from Detroit, geographically and economically. Note that if this did happen some neighbourhood would get hit hard while others would remain unaffected. Don't buy a house in a marginal neighbourhood.

Yes, you'll probably have higher expenses as a homeowner - maintenance, property tax, etc. These need to get figured into your calculations as to how much home you can afford. Do not be afraid to buy a small home so long as it is in a good neighbourhood.

So, to sum up: the heat may come out of the real estate market but if you want to own a house it is unlikely to get more affordable. Get in now and if your income goes up you can move up. But getting into "the game" as early as possible is your best bet. All IMO.

posted by GuyZero at 11:58 AM on March 11, 2008

As an example I have several neighbours who live in houses worth over $700K in Toronto who probably pay a fraction of what I pay - I would guess in the neighbourhood of $900 monthly - because they have lived there a long time. Based on their income alone it would literally be impossible for them to buy the house they currently live in. Or, as one California real estate blog put it: how can you afford to live in Palo Alto when you only make $125K? Buy the house in 1992.

Housing prices have increase much faster than earning or the cost of living in general so it's become relatively harder to buy a home. Some would say that this calls for a correction. I do not believe this to be the case - in places like Vancouver it's a simple case of supply and demand. Demand for Vancouver homes has outstripped supply and will continue to do so into the foreseeable future. This, IMO, leads me to conclude that even if the Vancouver economy went into the shitter house prices would remain high until things got so bad that there was a mass exodus out of the city. Vancouver is a long way from Detroit, geographically and economically. Note that if this did happen some neighbourhood would get hit hard while others would remain unaffected. Don't buy a house in a marginal neighbourhood.

Yes, you'll probably have higher expenses as a homeowner - maintenance, property tax, etc. These need to get figured into your calculations as to how much home you can afford. Do not be afraid to buy a small home so long as it is in a good neighbourhood.

So, to sum up: the heat may come out of the real estate market but if you want to own a house it is unlikely to get more affordable. Get in now and if your income goes up you can move up. But getting into "the game" as early as possible is your best bet. All IMO.

posted by GuyZero at 11:58 AM on March 11, 2008

Don't compare to some hypothetical future state, compare to what you'll be doing if you don't buy.

posted by winston at 12:11 PM on March 11, 2008

posted by winston at 12:11 PM on March 11, 2008

whereas your mortgage payments will only change based on interest rate changes which could go either way.

If a portion of your monthly check is escrow for taxes, that portion is also likely to increase over time.

posted by ROU_Xenophobe at 12:25 PM on March 11, 2008

If a portion of your monthly check is escrow for taxes, that portion is also likely to increase over time.

posted by ROU_Xenophobe at 12:25 PM on March 11, 2008

Don't try to time the market. Let's say you wait two more years and then buy. Prices could easily rise during those two years, and decline in the third year. Housing prices vary enough that you can't count on them going up or down in a short period of time, but in the long run they at least keep up with inflation.

Investing wisely is not about timing but instead about asset allocation. How much of your net worth will you be tying up in equity for your house? If you already have a significant amount of money invested in the stock market (including retirement funds), then buying real estate could help you diversify. If you put too much of your net worth into your house, you will be hit harder if the market takes a downward turn.

posted by burnmp3s at 12:46 PM on March 11, 2008

Investing wisely is not about timing but instead about asset allocation. How much of your net worth will you be tying up in equity for your house? If you already have a significant amount of money invested in the stock market (including retirement funds), then buying real estate could help you diversify. If you put too much of your net worth into your house, you will be hit harder if the market takes a downward turn.

posted by burnmp3s at 12:46 PM on March 11, 2008

If a portion of your monthly check is escrow for taxes, that portion is also likely to increase over time.

It depends on tax increases in your local area as well as how they assess the value of your house. Prop 13 in California limits property tax increases quite severely while Toronto has seen both increases in the mill rate as well as using a "current value" assessment scheme which sees the value of you house increase every year.

But unlike the mortgage, which can be considered as an inventment (for the principal portion) taxes are a pure expense. I personally consider the separately regardless of how the money actually gets from A to B. In some cases (Ontario) you get a tax credit for property taxes though and I expect it would be the same in most areas on the basis that you don't pay taxes on taxes. But IANATA.

Don't try to time the market.

Sage advice.

posted by GuyZero at 1:20 PM on March 11, 2008

It depends on tax increases in your local area as well as how they assess the value of your house. Prop 13 in California limits property tax increases quite severely while Toronto has seen both increases in the mill rate as well as using a "current value" assessment scheme which sees the value of you house increase every year.

But unlike the mortgage, which can be considered as an inventment (for the principal portion) taxes are a pure expense. I personally consider the separately regardless of how the money actually gets from A to B. In some cases (Ontario) you get a tax credit for property taxes though and I expect it would be the same in most areas on the basis that you don't pay taxes on taxes. But IANATA.

Don't try to time the market.

Sage advice.

posted by GuyZero at 1:20 PM on March 11, 2008

I would do some more research on Vancouver housing prices to validate that they have been "increasing about 10% a year for the past decade." This could well be, but it means the average house has more or less tripled in 10 years.

If this is the case, you could well be buying at the peak of the market, so that's one reason to be cautious. As noted, trying to time the market is a bad idea. But thinking of your house as an investment you're trying to make a killing on is a bad idea as well. People who do this often try to buy the most house they can buy, on the theory that the upside will be that much better. But so's the downside.

So, buy a house because you need a roof over your head. Be conservative, buy the minimum house you need to be comfortable, not an oversized speculative house you won't even be able to furnish. Buy a house you can improve to neighborhood standards; don't buy a house that's already the best in the neighborhood. Put down at least 20% in down payment and preferably more. Get a conventional 20-year mortgage.

posted by beagle at 1:40 PM on March 11, 2008 [1 favorite]

If this is the case, you could well be buying at the peak of the market, so that's one reason to be cautious. As noted, trying to time the market is a bad idea. But thinking of your house as an investment you're trying to make a killing on is a bad idea as well. People who do this often try to buy the most house they can buy, on the theory that the upside will be that much better. But so's the downside.

So, buy a house because you need a roof over your head. Be conservative, buy the minimum house you need to be comfortable, not an oversized speculative house you won't even be able to furnish. Buy a house you can improve to neighborhood standards; don't buy a house that's already the best in the neighborhood. Put down at least 20% in down payment and preferably more. Get a conventional 20-year mortgage.

posted by beagle at 1:40 PM on March 11, 2008 [1 favorite]

If I were making a bet, I'd bet that housing prices will rise over the next 5-10 years (or longer) in desirable urban areas like Vancouver (outer suburbs and declining cities are a different matter). Over that time frame, there may be a period where prices decline, I personally wouldn't bet on it. In your case, I think you are more likely to spend 10% more on a house if you wait than you are to spend 10% less.

It is possible to make a good case for renting, rather than becoming a home owner, but if you intend to own a home, don't try to time the market.

posted by Good Brain at 1:45 PM on March 11, 2008

It is possible to make a good case for renting, rather than becoming a home owner, but if you intend to own a home, don't try to time the market.

posted by Good Brain at 1:45 PM on March 11, 2008

Vancouver resident chiming in. I'm with you on this one. It's true that buying to hold is a different animal entirely, than speculating. That said, it sure would be better to buy after a market correction than just before one.

Here are some links to blogs on the local market.

Financial Planning and Personal Sanity

Vancouver Condo Info

The Best Real Estate Anywhere

Real Estate Talks

All are Vancouver-centric, and have plenty of astute comments on them, many of which suggest that we are at the precipice of a serious market correction. Look particularly for the graphs on the Financial Planning site. You will find support for your argument there.

So to answer your question should we buy?, in my opinion, not now, it's much cheaper to rent, no question.

posted by lunaazul at 2:19 PM on March 11, 2008

Here are some links to blogs on the local market.

Financial Planning and Personal Sanity

Vancouver Condo Info

The Best Real Estate Anywhere

Real Estate Talks

All are Vancouver-centric, and have plenty of astute comments on them, many of which suggest that we are at the precipice of a serious market correction. Look particularly for the graphs on the Financial Planning site. You will find support for your argument there.

So to answer your question should we buy?, in my opinion, not now, it's much cheaper to rent, no question.

posted by lunaazul at 2:19 PM on March 11, 2008

Can you afford a place you'll want to stay in, and one that's in reasonable shape?

Housing prices are sure to drop significantly when interest rates rise. But that will make a loan more expensive. Vancouver will be hot at least until the Olympics, but there is no such thing as certainty in the housing market. It ends up being a partially emotional decision.

posted by gesamtkunstwerk at 2:21 PM on March 11, 2008

Housing prices are sure to drop significantly when interest rates rise. But that will make a loan more expensive. Vancouver will be hot at least until the Olympics, but there is no such thing as certainty in the housing market. It ends up being a partially emotional decision.

posted by gesamtkunstwerk at 2:21 PM on March 11, 2008

Beagle, it would totally fair to assume that the average Vancouver house has tripled in price since 10 years ago. Western Canada is really coming into it's own, attracting lots of people from elsewhere, and Vancouver is the jewel of this side of the country.

larry, I've been asking myself similar questions about buying in Calgary, and we seem to be in similar boats regarding money and intent, so I'll share my conclusion with you:

Renting is for suckers who can't afford down payments. If you have any reasonable expectation that your house will increase in sale value over the period you are likely to live there, buy that house. Yeah, it's always a partially emotional decision, and you can never be sure of anything. But if you have a decent, sturdy place in a central, convenient neighborhood of Canada's awesomest city, you've got a reasonable expectation of security. The bubble is going to retract soon, however - it simply has to. There are only a finite number of people who want to move to Vancouver, and when they stop coming in droves, bunches of people in the housing industry will move to the next boom town and leave their empty places behind to lower values.

Get insurance that covers your mortgage in case of health or employment emergency, and make sure you educate yourself about the other costs of home ownership so your budget doesn't get blown the first time your toilet explodes.

posted by chudmonkey at 4:10 PM on March 11, 2008

larry, I've been asking myself similar questions about buying in Calgary, and we seem to be in similar boats regarding money and intent, so I'll share my conclusion with you:

Renting is for suckers who can't afford down payments. If you have any reasonable expectation that your house will increase in sale value over the period you are likely to live there, buy that house. Yeah, it's always a partially emotional decision, and you can never be sure of anything. But if you have a decent, sturdy place in a central, convenient neighborhood of Canada's awesomest city, you've got a reasonable expectation of security. The bubble is going to retract soon, however - it simply has to. There are only a finite number of people who want to move to Vancouver, and when they stop coming in droves, bunches of people in the housing industry will move to the next boom town and leave their empty places behind to lower values.

Get insurance that covers your mortgage in case of health or employment emergency, and make sure you educate yourself about the other costs of home ownership so your budget doesn't get blown the first time your toilet explodes.

posted by chudmonkey at 4:10 PM on March 11, 2008

One thing you can look at is the price-rent ratio. This compares the price for buying a home and renting a similar home in a similar neighborhood. The ratio is the cost of the home divided by the annual rent for an equivalent home. Annual rent is just the monthly rent times 12. You can research this yourself in the real estate ads. A ratio of 9 means houses are very cheap. A ratio of 23 or higher means houses are very expensive and you are probably better off renting. The price-rent ratio is only a rough gauge like the body mass index for obesity, but it can at least tell you whether your market is vastly over or under priced.

posted by JackFlash at 5:12 PM on March 11, 2008

posted by JackFlash at 5:12 PM on March 11, 2008

Vancouverite here. The Vancouver market has doubled or tripled in the past 10 years, depending on where you live. Friends of mine bought their house for $325k around 2000, spent $150k renovating and it is now worth $1.1M. However, there is now a large spread between what you would pay in rent and what you would pay on a mortgage. And the Vancouver market has declined by 40-50% many times in the past 100 years, including (I believe) four times in the 1980s and 1990s.

No one can tell you what the market is going to do. But you might consider whether you might be forced to sell at some point, due to death, divorce, job transfer, etc. If there is a correction (of even 20%), would you be upside-down on the mortgage? Would buying wipe out your savings, leaving you unable to pay the mortgage during a job loss or illness? Could you stomach seeing the market dive 20-40% or would you panic sell?

My advice? If you decide to buy, make sure it's a property you can add value to or that is up and coming. That will at least shield you from some market conditions. We bought a completely wrecked place, worked hard to renovate it, and have seen that add value. It's also across the street from two ugly, noisy construction sites. When the construction ends, that will greatly increase our value. Moreover, we read city zoning plans and saw that a new grocery store, major drug store and various other retail developments would be coming into the neighbourhood, further increasing value. So, if you can find a situation like that, you may be okay, even if the market drops, because your position *relative* to other properties will increase. YMMV.

posted by acoutu at 5:38 PM on March 11, 2008

No one can tell you what the market is going to do. But you might consider whether you might be forced to sell at some point, due to death, divorce, job transfer, etc. If there is a correction (of even 20%), would you be upside-down on the mortgage? Would buying wipe out your savings, leaving you unable to pay the mortgage during a job loss or illness? Could you stomach seeing the market dive 20-40% or would you panic sell?

My advice? If you decide to buy, make sure it's a property you can add value to or that is up and coming. That will at least shield you from some market conditions. We bought a completely wrecked place, worked hard to renovate it, and have seen that add value. It's also across the street from two ugly, noisy construction sites. When the construction ends, that will greatly increase our value. Moreover, we read city zoning plans and saw that a new grocery store, major drug store and various other retail developments would be coming into the neighbourhood, further increasing value. So, if you can find a situation like that, you may be okay, even if the market drops, because your position *relative* to other properties will increase. YMMV.

posted by acoutu at 5:38 PM on March 11, 2008

Have a look at incomes versus prices to get a handle on affordability. If the average income can't buy the median house price, figure on little growth ahead (although if it is vastly out of whack, a crash might occur, as in some Californian areas).

In the last decade or two some things happened that radically altered the affordability of housing. One was the increased participation of women in the workforce. This alone supported a doubling of house prices as more and more families could afford higher mortgages. Another was amazingly low interest rates. These probably allowed another doubling of house prices. In both cases nobody is much better off, as the greater availability of money lead directly to higher prices, as people will tend to pay as much as they can afford for housing, and even if you won't the market has gone up to force you.

Both these events were one shot deals, unless you have an extra spouse you can send out to work ;-) so I wouldn't expect another price doubling unless you can think of another macro change to support it.

The impact of these changes affected different areas to different degrees, and at different times. If Vancouver has property prices that lagged other areas, it may continue booming, but I don't think that is the case.

The other thing to consider is that most real estate markets don't crash, they just stay flat for a decade as inflation brings high prices back into line.

If this is the case where you are, then waiting might not do you much good either.

The best approach would probably be to find a house you can comfortably afford and wish to live in long term. With this approach it doesn't matter what the property market does.

posted by bystander at 5:59 PM on March 11, 2008

In the last decade or two some things happened that radically altered the affordability of housing. One was the increased participation of women in the workforce. This alone supported a doubling of house prices as more and more families could afford higher mortgages. Another was amazingly low interest rates. These probably allowed another doubling of house prices. In both cases nobody is much better off, as the greater availability of money lead directly to higher prices, as people will tend to pay as much as they can afford for housing, and even if you won't the market has gone up to force you.

Both these events were one shot deals, unless you have an extra spouse you can send out to work ;-) so I wouldn't expect another price doubling unless you can think of another macro change to support it.

The impact of these changes affected different areas to different degrees, and at different times. If Vancouver has property prices that lagged other areas, it may continue booming, but I don't think that is the case.

The other thing to consider is that most real estate markets don't crash, they just stay flat for a decade as inflation brings high prices back into line.

If this is the case where you are, then waiting might not do you much good either.

The best approach would probably be to find a house you can comfortably afford and wish to live in long term. With this approach it doesn't matter what the property market does.

posted by bystander at 5:59 PM on March 11, 2008

As an example I have several neighbours who live in houses worth over $700K in Toronto who probably pay a fraction of what I pay - I would guess in the neighbourhood of $900 monthly - because they have lived there a long time.

Take a very close look at property taxes in your preferred neighbourhood. Toronto's property tax mill rate is below 0.75%, an extraordinarily low number. Other municipalities around Ontario have mill rates in the 2-3% range, and that makes buying much less attractive. In many places, a $500,000 home costs $1,000/month in taxes alone!

My property tax rant from earlier this year.

posted by Chuckles at 6:50 PM on March 11, 2008

Take a very close look at property taxes in your preferred neighbourhood. Toronto's property tax mill rate is below 0.75%, an extraordinarily low number. Other municipalities around Ontario have mill rates in the 2-3% range, and that makes buying much less attractive. In many places, a $500,000 home costs $1,000/month in taxes alone!

My property tax rant from earlier this year.

posted by Chuckles at 6:50 PM on March 11, 2008

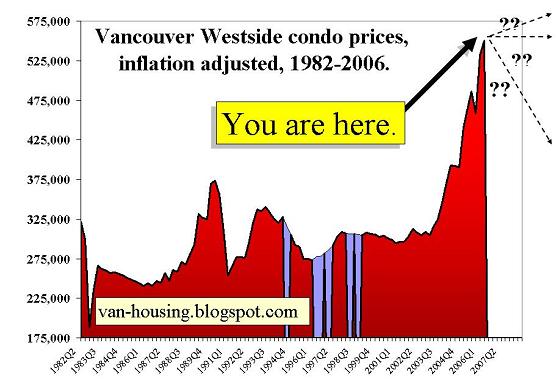

I won't candycoat: it is a criminally stupid time to buy real estate in Vancouver. Read some of those blogs linked above, look at the charts. Timing the market is difficult and unwise, as mentioned, but that doesn't mean one should throw out the evidence at hand entirely.

The Olympics in 2010 are a wildcard, but if there is anything less than a 20-30% correction downwards in the next three years, troughing out to about 4 or 5 years, I'll eat my damn hat. Here's a graph from the late, lamented van-housing blog. It's not difficult to interpret.

posted by stavrosthewonderchicken at 10:47 PM on March 11, 2008 [3 favorites]

The Olympics in 2010 are a wildcard, but if there is anything less than a 20-30% correction downwards in the next three years, troughing out to about 4 or 5 years, I'll eat my damn hat. Here's a graph from the late, lamented van-housing blog. It's not difficult to interpret.

{kind=link}

posted by stavrosthewonderchicken at 10:47 PM on March 11, 2008 [3 favorites]

It's not difficult to interpret.

THe price of oil has done basically the same thing. Why? Demand. And that demand will not abate once the Olympics are over. Here's data on Vancouver's population growth. And a chart of % population growth by year. If you look at this graph I interpret it as showing that in 2001 the prime home buying age category reached a percentage wise (and probably absolute, but the graphs don't show that) peak. Thus the huge demand for homes over the last few years and the run-up in prices.

The supply of housing in Vancouver is fairly inelastic - condos are being put up at a good clip, but the stock of single-family homes remains largely static. Vancouver, proper, is completely hemmed in. And there will always be demand for homes in the core or in goold "old" neighbourhood, like around UBC or in North Van versus the outlying 'burbs. Demand is going in only one direction - up. Will growth continue at the same rate? Probably not. But I doubt, barring unforseen changes to Vancouver, that there will be a major drop in housing prices. Unless the economy in general goes off and interest rates rise, which will suck the life out of every housing market in the country.

posted by GuyZero at 5:09 AM on March 12, 2008

THe price of oil has done basically the same thing. Why? Demand. And that demand will not abate once the Olympics are over. Here's data on Vancouver's population growth. And a chart of % population growth by year. If you look at this graph I interpret it as showing that in 2001 the prime home buying age category reached a percentage wise (and probably absolute, but the graphs don't show that) peak. Thus the huge demand for homes over the last few years and the run-up in prices.

The supply of housing in Vancouver is fairly inelastic - condos are being put up at a good clip, but the stock of single-family homes remains largely static. Vancouver, proper, is completely hemmed in. And there will always be demand for homes in the core or in goold "old" neighbourhood, like around UBC or in North Van versus the outlying 'burbs. Demand is going in only one direction - up. Will growth continue at the same rate? Probably not. But I doubt, barring unforseen changes to Vancouver, that there will be a major drop in housing prices. Unless the economy in general goes off and interest rates rise, which will suck the life out of every housing market in the country.

posted by GuyZero at 5:09 AM on March 12, 2008

People thought the American real estate market would go up forever, too. Lots of people didn't see the BC real estate busts in the early 80's and early 90's coming either. And lots of people have pulled out the 'they're not making any more land' chestnut, too.

Unless the economy in general goes off

Heard of the pine beetle? The 80% die-off? BC's in for some mighty rough times in the coming years.

Whatever, though. I believe you are precisely wrong, but this is an argument that has been going on for years, and only time will tell which of us has it. Let's meet back here in a year or two and see who was closer to right. I still say it'd be a fool's wager to make a $600,000 bet when all the signs, whether you're the prototypical bull or bear, point to nothing but grief. A study of history will always behoove us more than prognosticatory handwaving.

posted by stavrosthewonderchicken at 5:22 AM on March 12, 2008

Unless the economy in general goes off

Heard of the pine beetle? The 80% die-off? BC's in for some mighty rough times in the coming years.

Whatever, though. I believe you are precisely wrong, but this is an argument that has been going on for years, and only time will tell which of us has it. Let's meet back here in a year or two and see who was closer to right. I still say it'd be a fool's wager to make a $600,000 bet when all the signs, whether you're the prototypical bull or bear, point to nothing but grief. A study of history will always behoove us more than prognosticatory handwaving.

posted by stavrosthewonderchicken at 5:22 AM on March 12, 2008

JackFlash: One thing you can look at is the price-rent ratio.

The ">Vancouver Real Estate Bubble Uberpost on the Financial Planning and Personal Sanity blog includes a graph showing the price-rent ratio for a single-family house in Greater Vancouver over time. It's gone from 17 in 2000 to 27 today.

The source of the data isn't given, unfortunately.

posted by russilwvong at 9:23 PM on March 12, 2008

The ">Vancouver Real Estate Bubble Uberpost on the Financial Planning and Personal Sanity blog includes a graph showing the price-rent ratio for a single-family house in Greater Vancouver over time. It's gone from 17 in 2000 to 27 today.

{kind=link}

The source of the data isn't given, unfortunately.

posted by russilwvong at 9:23 PM on March 12, 2008

Just ran across this this morning, thought it might be relevant. A taste:

The Toronto Sun reports from Canada. “The cost of carrying a home hit highs not seen since 1990 — when a real estate bubble burst — the price pressure will ease as our hot real estate market cools off, house price gains shrink and mortgage rates drop. Still, no one’s talking crash, 1989-style. Real estate has been on a roll for the past decade, enjoying record growth, which is why affordability is getting further and further out of reach.”posted by stavrosthewonderchicken at 7:47 PM on March 16, 2008

“The latest housing affordability numbers by RBC Economics show that affordability in the final quarter of 2007 deteriorated everywhere in this country, except Alberta, where a cooling off of a feverish market is already under way.”

“In Toronto, where the market is now showing signs of a slowdown, it took 53% of pre-tax income to carry the cost of a standard two-storey home, priced at $476,000. That’s $3,089 a month to pay the mortgage, utilities and property taxes.”

“Vancouver, meanwhile, it still the most expensive place to own a home, with a detached bungalow eating up a whopping 74% of pre-tax income in the final quarter of 2007 — much higher than the 63.1% Toronto’s market cost in 1989, when the bubble burst.”

“Calgary took 42% of pre-tax income, Montreal 37% and Ottawa 32%.”

« Older It's hard to be cool. Then why is it so hard to... | Is there another method of placing bumper stickers... Newer »

This thread is closed to new comments.

posted by mmascolino at 11:24 AM on March 11, 2008