Safe place to park my 401k?

February 1, 2017 12:40 PM Subscribe

So with all that's going on, this seems like a selfish question to ask, but I'm worried about my retirement account. I have a 401k that's a mix of mostly index funds and a few individual stocks.

I'm assuming Trump is going to sink the economy sooner rather than later based on his current performance. I'd like to shift half of the total fund into something more recession proof than what I currently have.

Normally I'd go with a bond fund, but that's reverse linked to the interest rate, and I wouldn't be surprised to see that go up if our credit starts to dry up and/or a trade war gets started.

I'm 20 years away from retirement, so I have no immediate need to draw from this fund.

I'm assuming Trump is going to sink the economy sooner rather than later based on his current performance. I'd like to shift half of the total fund into something more recession proof than what I currently have.

Normally I'd go with a bond fund, but that's reverse linked to the interest rate, and I wouldn't be surprised to see that go up if our credit starts to dry up and/or a trade war gets started.

I'm 20 years away from retirement, so I have no immediate need to draw from this fund.

20 years to go? Leave. It. Be. Humans are terrible at predicting the future and if you aren't going to need to use the money (you aren't, you basically can't even touch it) you don't need to "recession proof" it.

posted by praemunire at 12:49 PM on February 1, 2017 [8 favorites]

posted by praemunire at 12:49 PM on February 1, 2017 [8 favorites]

You have 20 years. You can therefore tolerate a lot of risk. Even Great Depression of 1929 level risk. Just do a target date fund at Vanguard.

posted by zippy at 12:49 PM on February 1, 2017 [9 favorites]

posted by zippy at 12:49 PM on February 1, 2017 [9 favorites]

I'm hardly an expert but I took a big chunk out of my index funds right before the inauguration. The market is extremely high post-Obama and I don't want quite so much money in something that has a huge potential to drop. I moved it into some lightly managed target retirement-type funds that do the diversifying for me.

And it makes me sick to my stomach that I did it, but I hedged by moving a small amount of money into energy and private prison stocks. Human despair is a growth industry.

In related news, I found a site called Personal Capital just yesterday that I would describe as Mint for investments. It does a really good job of breaking down where your money actually is and what kind of things you need to look for.

posted by phunniemee at 12:54 PM on February 1, 2017 [1 favorite]

And it makes me sick to my stomach that I did it, but I hedged by moving a small amount of money into energy and private prison stocks. Human despair is a growth industry.

In related news, I found a site called Personal Capital just yesterday that I would describe as Mint for investments. It does a really good job of breaking down where your money actually is and what kind of things you need to look for.

posted by phunniemee at 12:54 PM on February 1, 2017 [1 favorite]

And even if you are terrible at predicting, you can still do ok if you stay in long term. What if You Only Invested at Market Peaks?

posted by fings at 12:55 PM on February 1, 2017 [2 favorites]

posted by fings at 12:55 PM on February 1, 2017 [2 favorites]

I've redirected new contributions away from stocks since early January. I have been considering shifting away from a relatively aggressive stock market exposure (that's done very well) over the last 4 years.

I think there is still upside for stocks as the euphoria over deregulation will fuel a fair bit of new investment. Morally I'm not sure I wish to benefit from it however. But longer term -- I'm thinking a year or so -- we are so long overdue for an organic correction and interest rates must go up, never mind global instability and trade wars.

I'm working on a ten year horizon that just got even shorter, and now includes checking out retirement abroad.

posted by spitbull at 1:29 PM on February 1, 2017

I think there is still upside for stocks as the euphoria over deregulation will fuel a fair bit of new investment. Morally I'm not sure I wish to benefit from it however. But longer term -- I'm thinking a year or so -- we are so long overdue for an organic correction and interest rates must go up, never mind global instability and trade wars.

I'm working on a ten year horizon that just got even shorter, and now includes checking out retirement abroad.

posted by spitbull at 1:29 PM on February 1, 2017

A 20 year horizon means don't even think about trying to time the market, in my book. In the past 20 years there have been several major calamities (9/11, Lehman, multiple tech busts, etc.) and yet, if you had put your money on the sidelines in 1997, you'd be sad about it now.

posted by Mid at 4:46 PM on February 1, 2017 [2 favorites]

posted by Mid at 4:46 PM on February 1, 2017 [2 favorites]

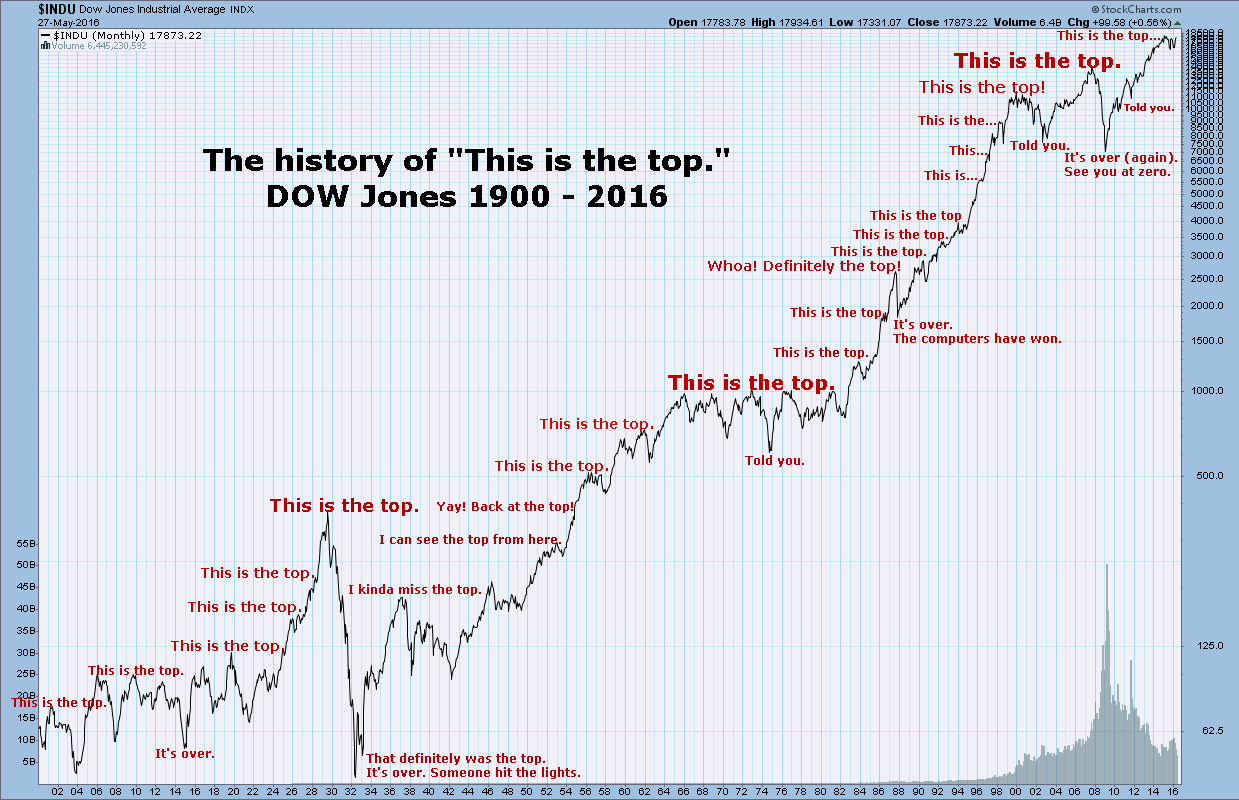

...if you had put your money on the sidelines in 1997, you'd be sad about it now.

Exactly. Here's a companion chart to Mid's, amusingly annotated with all the times the Dow hit "This Is the Top" territory.

posted by Short Attention Sp at 5:51 AM on February 2, 2017 [2 favorites]

Exactly. Here's a companion chart to Mid's, amusingly annotated with all the times the Dow hit "This Is the Top" territory.

{kind=link}

posted by Short Attention Sp at 5:51 AM on February 2, 2017 [2 favorites]

The Financial Planning Firm I use out put a 2017 outlook on their site. Here it is (PDF), if anyone is interested.

posted by getawaysticks at 7:57 AM on February 2, 2017

posted by getawaysticks at 7:57 AM on February 2, 2017

Best answer: You don't know Trump will sink the economy. He could be impeached within 2 years. Or maybe deregulation could be good for business. That said, we're due for a natural correction as we've been riding a bull market since 2009. But the correction may not come for years for all we know.

My point is you need to decide a reasonable asset allocation that will enable you to mentally ride the market's bumps without jumping in and out of the market for speculative reasons.

For me that's a 50/50 stock/ bond portfolio. If your asset allocation causes you lost sleep, you're too aggressively invested.

posted by LoveHam at 11:38 AM on February 2, 2017

My point is you need to decide a reasonable asset allocation that will enable you to mentally ride the market's bumps without jumping in and out of the market for speculative reasons.

For me that's a 50/50 stock/ bond portfolio. If your asset allocation causes you lost sleep, you're too aggressively invested.

posted by LoveHam at 11:38 AM on February 2, 2017

« Older How to use the Android text expander Texpand Pro... | Help for a Team told to sponsor podcasts Newer »

This thread is closed to new comments.

I did specifically ask him: well, what about some sort of terrible financial collapse? His answer was: yes, that could happen, but as long as you're diversified, the only type of collapse that will wipe out your retirement is the type where whether or not you have a retirement account ceases to matter (i.e. we don't use the dollar anymore so anything invested in dollars is worthless, nuclear holocaust, etc.).

posted by rainbowbrite at 12:47 PM on February 1, 2017 [12 favorites]