Apply for a loan to help my credit?

June 23, 2007 9:05 PM Subscribe

I am in my 20's, have no debt and have no need for a loan; should I get one anyways to help my credit?

I have a high credit score, and I pay off my credit cards monthly; but I have never taken out a loan, not even student loans... I worry this will hurt me when the time comes to apply for a car loan, home loan, etc...

What kind of loan should I apply for? I would be able to pay off any loan I apply for, but don't know where to begin... I don't need a car nor am I looking to buy a house; so car/home loans are out... I have only heard of personal loans but don't know if this is the best option...

Whatever loan I decide to get would be placed in a savings account accruing 4.5%...

Any help is will be GREATLY appreciated...

I have a high credit score, and I pay off my credit cards monthly; but I have never taken out a loan, not even student loans... I worry this will hurt me when the time comes to apply for a car loan, home loan, etc...

What kind of loan should I apply for? I would be able to pay off any loan I apply for, but don't know where to begin... I don't need a car nor am I looking to buy a house; so car/home loans are out... I have only heard of personal loans but don't know if this is the best option...

Whatever loan I decide to get would be placed in a savings account accruing 4.5%...

Any help is will be GREATLY appreciated...

Whatever loan you get will probably be at a worse interest rate than 4.5%, so you'll be losing money as you pay off your loan. If you're going to do this, put it in something with a higher risk but higher potential benefits, like stocks or mutual funds. I wouldn't do this, though. I was in the same situation as you until I bought my car, and I had no problem getting a good loan. As long as your credit score is high, you've really got nothing to worry about. You might want to sit down with someone at your bank and see if they have any more constructive ideas on building your credit, but I think you're in a good situation right now.

If you are really bent on getting a loan just for laughs, though, make it a big one and send me a check. My girlfriend and I are trying to buy a house together, and we could use the extra money for the down payment, to cover closing costs, or to buy new appliances and bathroom fixtures. If you decide to go this route, my e-mail's in the profile.

posted by infinitywaltz at 9:13 PM on June 23, 2007

If you are really bent on getting a loan just for laughs, though, make it a big one and send me a check. My girlfriend and I are trying to buy a house together, and we could use the extra money for the down payment, to cover closing costs, or to buy new appliances and bathroom fixtures. If you decide to go this route, my e-mail's in the profile.

posted by infinitywaltz at 9:13 PM on June 23, 2007

Best answer: Your current credit cards should be enough. If you have a high credit score like you say, and you've got income enough to show you can afford a loan, no lender is going to turn you down when you want to get a car or home. Keep in mind that lenders want desperately to loan money to you, it's how the make their money. You don't have to do take out unneeded loans to prove yourself to them.

posted by voidcontext at 9:14 PM on June 23, 2007

posted by voidcontext at 9:14 PM on June 23, 2007

Um, if you have a high credit score, I don't understand how having a loan (especially a loan for no reason whatsoever) would help you. If anything, I'd think the fact that you haven't needed a loan in the past would be a GOOD thing.

posted by echo0720 at 9:17 PM on June 23, 2007

posted by echo0720 at 9:17 PM on June 23, 2007

Credit history (which is part of your score) will in large part determine what you get in terms of loan offers.

You should absolutely NOT take a loan just because you think it might help you in the long run.

Save that money and invest it yourself; why do you need to pay someone else the interest? That way, when it comes time to buy that car you can do it with CASH. Or, when you're ready to buy that house, you can have a nice 20% down payment which will get you great terms on your mortgage.

You're doing things right; don't screw it up.

posted by ca_little at 9:18 PM on June 23, 2007

You should absolutely NOT take a loan just because you think it might help you in the long run.

Save that money and invest it yourself; why do you need to pay someone else the interest? That way, when it comes time to buy that car you can do it with CASH. Or, when you're ready to buy that house, you can have a nice 20% down payment which will get you great terms on your mortgage.

You're doing things right; don't screw it up.

posted by ca_little at 9:18 PM on June 23, 2007

My mom got me on her credit card as a secondary name when I was 16. I'm 19 now and am getting "pre-approved" offers for credit cards with credit lines over $10,000. I also qualify to take out loans for college which the lender had a hard time believing as I'm so young... It seems just having my name on a credit card (and now my own) helps a lot...

I wouldn't take out loans though, these can put a flag on your credit, whereas credit cards don't... Think about it, people use credit cards for convenience (mostly), not for borrowing money. Taking out a loan might look like you are in financial trouble because you "need" money.

Invest it, or put some in a CD.

posted by jammnrose at 9:34 PM on June 23, 2007

I wouldn't take out loans though, these can put a flag on your credit, whereas credit cards don't... Think about it, people use credit cards for convenience (mostly), not for borrowing money. Taking out a loan might look like you are in financial trouble because you "need" money.

Invest it, or put some in a CD.

posted by jammnrose at 9:34 PM on June 23, 2007

Best answer: You have a high credit score. If it ain't broke, don't fix it.

posted by Pater Aletheias at 10:06 PM on June 23, 2007

posted by Pater Aletheias at 10:06 PM on June 23, 2007

I might be tempted; I'd keep the amount comfortable and immediately put the money into into into some sort of mid-term treasury note. Establishing a rapport with yer friendly neighborhood loan officer is always handy, regardless of credit score.

posted by RavinDave at 10:16 PM on June 23, 2007

posted by RavinDave at 10:16 PM on June 23, 2007

Best answer: I think it's a bad idea. If your score is high already, don't mess with it.

Taking out loans seems like something you might do to repair a bad credit score, but if your score is already good, it can only hurt you, I'd think.

FWIW, I was like you -- no loans, for anything -- and didn't have any trouble getting a good rate the first time I bought a car and financed it.

posted by Kadin2048 at 10:19 PM on June 23, 2007

Taking out loans seems like something you might do to repair a bad credit score, but if your score is already good, it can only hurt you, I'd think.

FWIW, I was like you -- no loans, for anything -- and didn't have any trouble getting a good rate the first time I bought a car and financed it.

posted by Kadin2048 at 10:19 PM on June 23, 2007

Best answer: I am from Canada, so this advice may not apply. Could you take out a loan for an IRA? If you borrowed $5,000 and were in a 25% tax bracket, you would receive a tax refund for $1250. If you paid the loan back in one year at 8% interest, you would pay $400 in interest. You would still be up $850. This would allow you to put money into your IRA faster than you might have otherwise. For example, if you invest $5k this year and it averages 7% returns for 40 years, you'll make about $75k. But if you invested it for just 39 years instead, you'd only make $70k. So the value of investing one year earlier is $5k. You gain access to that for the cost of $400 -- and you get some extra credit history.

posted by acoutu at 10:30 PM on June 23, 2007

posted by acoutu at 10:30 PM on June 23, 2007

I wouldn't take out loans though, these can put a flag on your credit, whereas credit cards don't... Think about it, people use credit cards for convenience (mostly), not for borrowing money. Taking out a loan might look like you are in financial trouble because you "need" money.

Going to disagree. People who use credit cards (and maintain a interest bearing balance month to month) are using the line of credit because they do essentially need a loan. They use the card (and keep a balance and pay interest) because the cash wasn't there in the first place. A revolving line of credit (a credit card) is actually an unsecured loan. Racking up credit card debt actually "appears" worse than taking a secured loan like a car note or a mortgage. Not many credit card consumers, at least in the US, pay their entire credit card balance off every month. It's trending upwards as well, looking over the last 5 years and 8 quarters. Americans keep using their credit cards and carrying the debt. MrBCID is doing it right and likely in the minority as far as that goes.

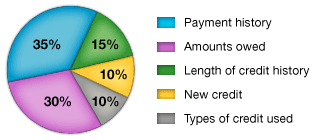

To MrBCID, don't worry about taking out a loan. It's not going to foster your credit worthiness. Attaching debt to your credit history isn't the answer. Keep doing what you're doing. Keep the credit card balances low, keep paying them off entirely, save up a nestegg in the meantime, and relax. If you're still stressed out about raising the score, check out Fair Issac -- it explains what goes into your credit score and how each contributing factor is weighed, and how to raise your score.

posted by jerseygirl at 5:38 AM on June 24, 2007

Going to disagree. People who use credit cards (and maintain a interest bearing balance month to month) are using the line of credit because they do essentially need a loan. They use the card (and keep a balance and pay interest) because the cash wasn't there in the first place. A revolving line of credit (a credit card) is actually an unsecured loan. Racking up credit card debt actually "appears" worse than taking a secured loan like a car note or a mortgage. Not many credit card consumers, at least in the US, pay their entire credit card balance off every month. It's trending upwards as well, looking over the last 5 years and 8 quarters. Americans keep using their credit cards and carrying the debt. MrBCID is doing it right and likely in the minority as far as that goes.

To MrBCID, don't worry about taking out a loan. It's not going to foster your credit worthiness. Attaching debt to your credit history isn't the answer. Keep doing what you're doing. Keep the credit card balances low, keep paying them off entirely, save up a nestegg in the meantime, and relax. If you're still stressed out about raising the score, check out Fair Issac -- it explains what goes into your credit score and how each contributing factor is weighed, and how to raise your score.

{kind=link}

posted by jerseygirl at 5:38 AM on June 24, 2007

Dont take out a loan man, if you have a high credit score and pay off your credit cards thats all a bank wants to see. The fact that you HAVE NEVER taken out a loan but still pay off your debts probably says more to a potential lender than if you had a bunch of loans. You know how to manage your money, so they know they will get paid.

posted by outsider at 10:18 AM on June 24, 2007

posted by outsider at 10:18 AM on June 24, 2007

Best answer: you might want to ask this question again at creditboards.com and read a couple of the discussions in the fatwallet.com forums.

posted by krautland at 12:36 PM on June 24, 2007

posted by krautland at 12:36 PM on June 24, 2007

also: there was a story in the WSJ this weekend about people taking out massive amounts of money from 0% teaster rates on new credit cards and plunking the money into high-interest savings accounts until the teaser rate expired, making a nice chunk in the process. read the article here.

the HSBC online savings account currently pays 5.05%. shop for the highest rate using a site like bankrate.com

posted by krautland at 12:40 PM on June 24, 2007

Best answer: Technically, the FICO scoring system DOES take factor in the different "types" of debt you have in your portfolio. Of the points you can earn, I heard here that there are points you can receive only for having at one point had an installment loan. (Not many points, only like 20.) According to that, you'd benefit in the long term by getting an installment loan, even if only for a short period.

But if you're really trying to game your FICO score, be aware that you will take a short-term hit for the inquiry (the fact that the bank has to run your credit to approve the loan) and, while you still have the loan open, for the usage (the percentage of available credit that you're using) (they calculate installment usage and revolving loan usage separately. One way to minimize this would be to immediately pay back 60%-70% of the loan, to get your usage to 30-40%).

So, to me, if you need a long-term score boost, don't mind a short-term score decline, and don't mind losing a small amount of interest, then yeah, take out a small loan, put it somewhere super-secure, pay it off in like 4 months, and there you go. On the other hand, if your score is >720, you probably already qualify for the best rates on everything, so it won't be worth your time and the interest you'd pay.

One random idea -- I think some "buy now, no interest for a year" loans to buy certain items, eg. Dell computers, get set up as installment loans. That might be a way to avoid paying interest, if the loan really were interest-free.

This is flat out wrong -- "I wouldn't take out loans though, these can put a flag on your credit, whereas credit cards don't... Think about it, people use credit cards for convenience (mostly), not for borrowing money. Taking out a loan might look like you are in financial trouble because you "need" money." In fact, credit card debt is a bigger red flag than bank loans. The underlying assumption is that only "irresponsible" people carry credit cards balances whereas almost everyone gets mortgages and student loans.

posted by salvia at 5:48 PM on June 24, 2007

But if you're really trying to game your FICO score, be aware that you will take a short-term hit for the inquiry (the fact that the bank has to run your credit to approve the loan) and, while you still have the loan open, for the usage (the percentage of available credit that you're using) (they calculate installment usage and revolving loan usage separately. One way to minimize this would be to immediately pay back 60%-70% of the loan, to get your usage to 30-40%).

So, to me, if you need a long-term score boost, don't mind a short-term score decline, and don't mind losing a small amount of interest, then yeah, take out a small loan, put it somewhere super-secure, pay it off in like 4 months, and there you go. On the other hand, if your score is >720, you probably already qualify for the best rates on everything, so it won't be worth your time and the interest you'd pay.

One random idea -- I think some "buy now, no interest for a year" loans to buy certain items, eg. Dell computers, get set up as installment loans. That might be a way to avoid paying interest, if the loan really were interest-free.

This is flat out wrong -- "I wouldn't take out loans though, these can put a flag on your credit, whereas credit cards don't... Think about it, people use credit cards for convenience (mostly), not for borrowing money. Taking out a loan might look like you are in financial trouble because you "need" money." In fact, credit card debt is a bigger red flag than bank loans. The underlying assumption is that only "irresponsible" people carry credit cards balances whereas almost everyone gets mortgages and student loans.

posted by salvia at 5:48 PM on June 24, 2007

I have no need for a loan; should I get one anyways to help my credit?

No.

posted by ikkyu2 at 5:52 PM on June 24, 2007

No.

posted by ikkyu2 at 5:52 PM on June 24, 2007

If you really want to take a short term loan out to prove you can pay it back it might as well be something that you can earn some scratch with. Search google for 'balance transfer arbitrage' or 'app-o-rama'.

The basic gist is, you take out a 0% balance transfers for 12 months credit card (or multiple). Migrate your credit lines to that card. Balance transfer to yourself (via check usually) and keep that money in a 5% interest bearing account. You don't lose principal and can pay back at anytime as long as you keep it liquid (no CDs or stocks) and you earn 5% on it. Yeah, you take a short term hit for getting the credit card(s) and taking out a big loan, but you get a big boost at the end when you pay back. Plus you get to sock away a couple $K in the bank.

I've been looking at this as a way to use my credit as an investment instead of the housing market.

posted by kookywon at 2:18 PM on June 26, 2007

The basic gist is, you take out a 0% balance transfers for 12 months credit card (or multiple). Migrate your credit lines to that card. Balance transfer to yourself (via check usually) and keep that money in a 5% interest bearing account. You don't lose principal and can pay back at anytime as long as you keep it liquid (no CDs or stocks) and you earn 5% on it. Yeah, you take a short term hit for getting the credit card(s) and taking out a big loan, but you get a big boost at the end when you pay back. Plus you get to sock away a couple $K in the bank.

I've been looking at this as a way to use my credit as an investment instead of the housing market.

posted by kookywon at 2:18 PM on June 26, 2007

kookywon, aren't those 0% balance transfer offers on credit cards? Those won't show up as installment loans. The OP already has credit cards. But if you know of 0% installment loans, I'll take one too. ;)

posted by salvia at 4:53 PM on June 26, 2007

posted by salvia at 4:53 PM on June 26, 2007

This thread is closed to new comments.

I had no trouble qualifying for a mortgage later.

posted by acoutu at 9:10 PM on June 23, 2007