Is the stock market's real long-term return just 2 percent?

May 12, 2013 5:42 AM Subscribe

I was looking around for information on long-term investment planning and I ran across this page, which says that after adjusting for inflation, long-term stock market returns are only 1.9% before taxes. The whole site seems to advocate this sort of really creepy gold fetishism that's been popping up lately, so my natural reaction is to dismiss it. But I still have doubts, and this plays into my anxieties about whether retirement savings is worthwhile at all. Help me debunk this? (Existential crisis inside.)

Okay, here's why I care:

At 10% return, retirement accounts just seem immensely practical. I'll have enough of a cushion that sometime in the future I can take a big hit in income and just use Roth contributions to cover the gap. Or (if I'm very, very careful, or the laws change) I could start a SEPP distribution before retirement age.

At 2%, the situation feels absolutely different. Not only will I need every penny of my retirement savings for, y'know, retirement, but non-market risks eat up all of my returns and then some. To start, I'm still at an age where there's a 25% chance I'll just drop dead before I can retire. Current politicians' talk of raising the retirement age increases that risk. And if the Baby Boomers are any indication, there's a definite chance that upon retirement, I'll become a reactionary and donate all my time to the election campaign for Ron Paul's grandson, which – ew. The expectation value of my savings shows such a loss that, God help me, retiring on catfood and government cheese looks almost prudent.

So yeah, I guess, followup question: If the returns really were just 2%, how could I feel more okay about retirement, and not that I'm throwing my money down a black hole?

Okay, here's why I care:

At 10% return, retirement accounts just seem immensely practical. I'll have enough of a cushion that sometime in the future I can take a big hit in income and just use Roth contributions to cover the gap. Or (if I'm very, very careful, or the laws change) I could start a SEPP distribution before retirement age.

At 2%, the situation feels absolutely different. Not only will I need every penny of my retirement savings for, y'know, retirement, but non-market risks eat up all of my returns and then some. To start, I'm still at an age where there's a 25% chance I'll just drop dead before I can retire. Current politicians' talk of raising the retirement age increases that risk. And if the Baby Boomers are any indication, there's a definite chance that upon retirement, I'll become a reactionary and donate all my time to the election campaign for Ron Paul's grandson, which – ew. The expectation value of my savings shows such a loss that, God help me, retiring on catfood and government cheese looks almost prudent.

So yeah, I guess, followup question: If the returns really were just 2%, how could I feel more okay about retirement, and not that I'm throwing my money down a black hole?

The page is clearly biased in favor of gold over stocks. History suggests that stocks will, over the long term, trounce gold. But gold bugs don't believe that, for some good reasons and for some bad reasons.

The trick is determining whether their good reasons (debased currency, etc.) are really sufficiently good to warrant skepticism about stocks.

I tend to think that their good arguments are not sufficient to abandon stocks, and I think gold bugger is more often than not useless and counterproductive.

posted by dfriedman at 5:58 AM on May 12, 2013

The trick is determining whether their good reasons (debased currency, etc.) are really sufficiently good to warrant skepticism about stocks.

I tend to think that their good arguments are not sufficient to abandon stocks, and I think gold bugger is more often than not useless and counterproductive.

posted by dfriedman at 5:58 AM on May 12, 2013

Here are some of Warren Buffett's thoughts on gold.

He, of course, is biased in favor of stocks; nonetheless, I think he presents better arguments against gold than the gold bugs present against stocks.

posted by dfriedman at 5:59 AM on May 12, 2013 [1 favorite]

He, of course, is biased in favor of stocks; nonetheless, I think he presents better arguments against gold than the gold bugs present against stocks.

posted by dfriedman at 5:59 AM on May 12, 2013 [1 favorite]

"Adjusted for inflation, the stock market's returns have been 5.85% a year on average since 1928" (versus 8.9% without that adjustment).

From the same article: "Stocks, as measured by the Standard & Poor's, have returned a mere 1.9% a year between Sept. 1, 2001 and Sept. 30, 2011"... but given that the Great Recession happened a mere five years ago, half of that 10-year period, duh!

In short, the goldbug page you read lies.

posted by IAmBroom at 6:10 AM on May 12, 2013 [6 favorites]

From the same article: "Stocks, as measured by the Standard & Poor's, have returned a mere 1.9% a year between Sept. 1, 2001 and Sept. 30, 2011"... but given that the Great Recession happened a mere five years ago, half of that 10-year period, duh!

In short, the goldbug page you read lies.

posted by IAmBroom at 6:10 AM on May 12, 2013 [6 favorites]

Not only that, but something happened in Sept 2001 that makes choosing that particular arbitrary starting point rather dubious.

posted by empath at 6:16 AM on May 12, 2013 [6 favorites]

posted by empath at 6:16 AM on May 12, 2013 [6 favorites]

Also, another way to think about this is to look at the performance of the S&P 500 over the past forty years.

In June of 1973, the S&P 500 was at 105.1. In May of 2013, the S&P 500 was at 1623.1.

Over forty years, its CAGR* was ~7.89%. That does not include dividends (which would increase the return) or inflation (which would decrease the return) or taxes and transaction costs (which would also decrease the return).

*CAGR = compound annual growth rate = {[(ending value / beginning value)] ^[(1 / # of years)] } - 1

posted by dfriedman at 6:16 AM on May 12, 2013 [1 favorite]

In June of 1973, the S&P 500 was at 105.1. In May of 2013, the S&P 500 was at 1623.1.

Over forty years, its CAGR* was ~7.89%. That does not include dividends (which would increase the return) or inflation (which would decrease the return) or taxes and transaction costs (which would also decrease the return).

*CAGR = compound annual growth rate = {[(ending value / beginning value)] ^[(1 / # of years)] } - 1

posted by dfriedman at 6:16 AM on May 12, 2013 [1 favorite]

I have no idea about the validity of the number per se, but remember that "adjusting for inflation" is a pretty big difference in the presentation of numbers when you're talking about long term investing. Indeed, one of the main reasons that we invest when we save, rather than stick the money in a mayonnaise jar, is so that the money we save today will be worth at least the same, if not more, in the future when we need it.

Conversely, one of the reasons we must pay interest when we borrow is that we'll repay in the future with dollars that are inflated relative to the ones we borrowed. There's a whole vocabulary about this in economics.

So depending on circumstances, 1-2% OVER INFLATION might not be so bad. A person investing on their $20,000 income in the '60s which grew to a $40-50k income in the 80s could live like someone with a $60-80k income in retirement because that's about the same level of real income over those periods (note: rough guesses on those numbers)

posted by randomkeystrike at 6:17 AM on May 12, 2013 [1 favorite]

Conversely, one of the reasons we must pay interest when we borrow is that we'll repay in the future with dollars that are inflated relative to the ones we borrowed. There's a whole vocabulary about this in economics.

So depending on circumstances, 1-2% OVER INFLATION might not be so bad. A person investing on their $20,000 income in the '60s which grew to a $40-50k income in the 80s could live like someone with a $60-80k income in retirement because that's about the same level of real income over those periods (note: rough guesses on those numbers)

posted by randomkeystrike at 6:17 AM on May 12, 2013 [1 favorite]

Also, the Dow Jones Industrial Average is a misleading proxy for the performance of stocks because it comprises only 30 stocks. Whereas, the S&P 500, comprising 500 stocks, encompasses something like 90% + of the stock market's market capitalization.

posted by dfriedman at 6:18 AM on May 12, 2013 [2 favorites]

posted by dfriedman at 6:18 AM on May 12, 2013 [2 favorites]

Best answer: The page you link to explicitly states that 1) it excludes dividends, and 2) it invents its own non-standard inflation calculation. Both moves are really weird and ideologically-motivated. (Excluding dividends is particularly strange since the author purports to prove that stock market gains are mostly nominal rather than real.) Ignore this web page.

posted by foursentences at 6:19 AM on May 12, 2013 [7 favorites]

posted by foursentences at 6:19 AM on May 12, 2013 [7 favorites]

I love the opening to Buffet's comments:

"What motivates most gold purchasers is their belief that the ranks of the fearful will grow. During the past decade that belief has proved correct."

posted by intermod at 6:20 AM on May 12, 2013 [2 favorites]

"What motivates most gold purchasers is their belief that the ranks of the fearful will grow. During the past decade that belief has proved correct."

posted by intermod at 6:20 AM on May 12, 2013 [2 favorites]

Best answer: I think it's a combination of 1) Ignoring dividend payouts (which, if reinvested, would get you another couple of percent) and 2) The extra 2.7% he added to the CPI, which seems pretty sketchy. That brings the 1.9% closer to the 5-7% number which is more in line with what you would expect over the long term. 10% is over-optimistic.

On previous, what foursentences said. Also the DJI is a terrible index, but if you want to show a chart that goes back to 1910 it's the only option.

posted by quaking fajita at 6:21 AM on May 12, 2013 [1 favorite]

On previous, what foursentences said. Also the DJI is a terrible index, but if you want to show a chart that goes back to 1910 it's the only option.

posted by quaking fajita at 6:21 AM on May 12, 2013 [1 favorite]

Response by poster: So the yield with the inflation adjustment, but also including dividends, is around 6%?

posted by aw_yiss at 6:23 AM on May 12, 2013

posted by aw_yiss at 6:23 AM on May 12, 2013

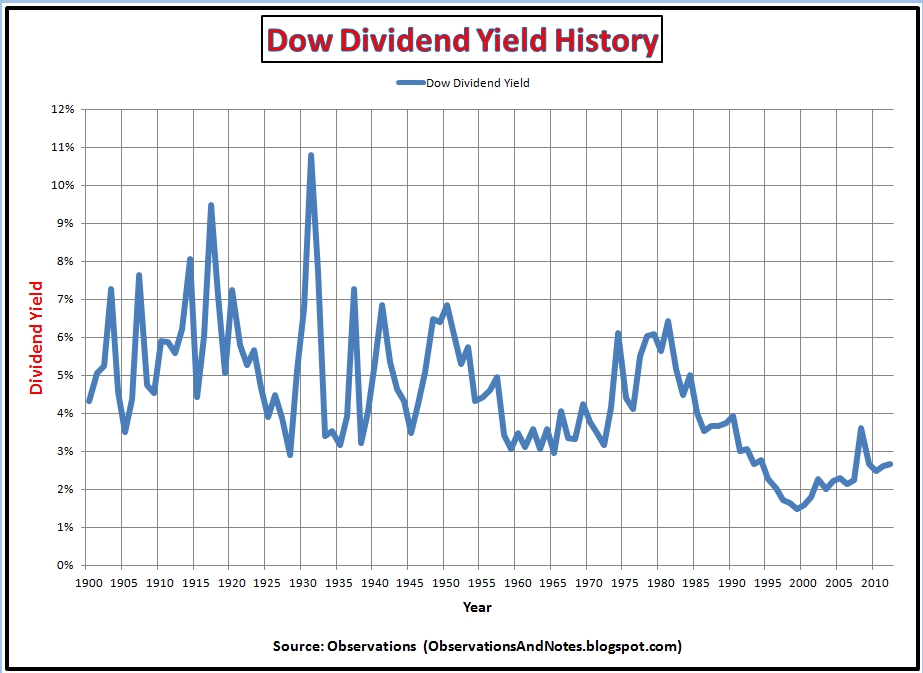

Best answer: With enough statistical obfuscation I could probably make the long term return on the DJIA look negative. Some of the tricks employed on the linked page:

-- They ignore dividends, which are a very real part of long term return. By way of disclosing that, they mention that "the dividend of the S&P is running near 2%". But, the analysis is not on the S&P, it's on the DJIA, so what's relevant is the dividend yield on the DJIA. The current overal dividend yield on DJIA stocks is 2.73%. But, since this is a long-term analysis, what's relevant is the long-term dividend yield on the DJIA, which over the period of this analysis is about 4.5%. (Slight guesstimation on my part off that chart, and granted it has been lower in recent years.)

--Then, the linked analysis is inflation-adjusted using a rate bumped up 2.7% from the CPI over the last 20 years ("Beginning 1994, I have added 2.7% per year to the government CPI number.") That's a bogus adjustment, which they base on somebody's opinion published in 2004.

--Then they take 0.8% for taxes, which a standard analysis would not do because actual tax rates vary by individual and should not be taken into account.

posted by beagle at 6:24 AM on May 12, 2013 [2 favorites]

-- They ignore dividends, which are a very real part of long term return. By way of disclosing that, they mention that "the dividend of the S&P is running near 2%". But, the analysis is not on the S&P, it's on the DJIA, so what's relevant is the dividend yield on the DJIA. The current overal dividend yield on DJIA stocks is 2.73%. But, since this is a long-term analysis, what's relevant is the long-term dividend yield on the DJIA, which over the period of this analysis is about 4.5%. (Slight guesstimation on my part off that chart, and granted it has been lower in recent years.)

{kind=link}

--Then, the linked analysis is inflation-adjusted using a rate bumped up 2.7% from the CPI over the last 20 years ("Beginning 1994, I have added 2.7% per year to the government CPI number.") That's a bogus adjustment, which they base on somebody's opinion published in 2004.

--Then they take 0.8% for taxes, which a standard analysis would not do because actual tax rates vary by individual and should not be taken into account.

posted by beagle at 6:24 AM on May 12, 2013 [2 favorites]

Best answer: So the yield with the inflation adjustment, but also including dividends, is around 6%?

It depends over what period you're calculating the yield. The returns before, say, 1970 are interesting but not that relevant in gauging the current momentum of growth and dividends.

But here is a pretty interesting historical analysis and graphic that says that if you invest a regular amount in an S&P index fund every month, reinvest all dividends, and calculate the inflation-adjusted yield, no matter when you started this strategy over the last 70 years, your net inflation-adjusted total return would have settled in between 3.5 and 5 percent.

He then compares this with "sticking your money under a mattress," which means it loses value on an inflation-adjusted basis, with yield settling in at around -4.5% (negative).

posted by beagle at 6:39 AM on May 12, 2013 [1 favorite]

It depends over what period you're calculating the yield. The returns before, say, 1970 are interesting but not that relevant in gauging the current momentum of growth and dividends.

But here is a pretty interesting historical analysis and graphic that says that if you invest a regular amount in an S&P index fund every month, reinvest all dividends, and calculate the inflation-adjusted yield, no matter when you started this strategy over the last 70 years, your net inflation-adjusted total return would have settled in between 3.5 and 5 percent.

He then compares this with "sticking your money under a mattress," which means it loses value on an inflation-adjusted basis, with yield settling in at around -4.5% (negative).

posted by beagle at 6:39 AM on May 12, 2013 [1 favorite]

even if it were true, you still need to save for retirement.

also, even if you visit the somewhat reputable internet sites dealing with investments, you'll get an unending stream of precise predictions based on a bunch of selectively chosen factors. it's hard to make sense of it all, even though it's relatively easy to deal with the math involved. if math were all that mattered, we'd all be rich.... it has many, many limits. i liken it to people discussing paint colors on a building while ignoring the building and the neighborhood in which is sits. which is more important? (warren buffet only looks the fundamentals... the foundations. screw the paint and flashy stuff. basic math is enough.)

the extremely long term trend lines in the value of the market reflect the effects of concentrated human enterprise, growth in the money supply, and general economic growth. it's unmistakable. how any one individual fares is noise, and a good part of it is zero sum.... to win for you, i have to lose, in the extreme short term.

The one thing to keep in mind is that "In the short term, the market is a voting machine. In the long term, it's a weighing machine.". All analysis in the time series depends on the interval you choose and the conditions on the boundaries. to some degree, it depends on your (or others) selected bias and what you HOPE to prove.

personally, i have always maintained that one of the best investments is yourself, your own initiative, enterprise, commerce, passions, earning power. here, anyway, there are few restrictions on what kind of enterprise and commerce you can pursue. nothing invalidates a retirement plan's significance more than being rich enough not to care.

posted by FauxScot at 6:40 AM on May 12, 2013

also, even if you visit the somewhat reputable internet sites dealing with investments, you'll get an unending stream of precise predictions based on a bunch of selectively chosen factors. it's hard to make sense of it all, even though it's relatively easy to deal with the math involved. if math were all that mattered, we'd all be rich.... it has many, many limits. i liken it to people discussing paint colors on a building while ignoring the building and the neighborhood in which is sits. which is more important? (warren buffet only looks the fundamentals... the foundations. screw the paint and flashy stuff. basic math is enough.)

the extremely long term trend lines in the value of the market reflect the effects of concentrated human enterprise, growth in the money supply, and general economic growth. it's unmistakable. how any one individual fares is noise, and a good part of it is zero sum.... to win for you, i have to lose, in the extreme short term.

The one thing to keep in mind is that "In the short term, the market is a voting machine. In the long term, it's a weighing machine.". All analysis in the time series depends on the interval you choose and the conditions on the boundaries. to some degree, it depends on your (or others) selected bias and what you HOPE to prove.

personally, i have always maintained that one of the best investments is yourself, your own initiative, enterprise, commerce, passions, earning power. here, anyway, there are few restrictions on what kind of enterprise and commerce you can pursue. nothing invalidates a retirement plan's significance more than being rich enough not to care.

posted by FauxScot at 6:40 AM on May 12, 2013

The answers given in this thread so far are right, as far as they go, but many of them (and your question) rely on the same crucial assumption: that the future will be like the past. Isn't there good reason to believe that isn't true?

What makes a stock a good investment? Since dividend payouts are now negligible (they weren't always), participants in the stock market, like participants in the housing market before them, rely on finding a "greater fool" to sell their stocks to at a profit. Historically, this has worked out well, for much the same reason that housing was a good investment for the Boomers: the combination of a demographic bulge, increases in productivity, and growing public acceptance of and participation in the market (driven, in the case of housing, in part by easily affordable mortgages provided to returning military members, and in the case of stocks, by IRA's and the decline of pensions) caused large, sustained price increases. But, as Herb Stein famously said, if something can't go on forever, it will stop. As the Boomers cash in their retirement accounts, and succeeding generations are both smaller and less able to invest (due to the economic recession, higher tax burdens, and the burden of paying for parents that have outlived their retirement savings), will there always be greater fools?

When you think about it, is it rational that unskilled consumers/investors should be able to sustainably generate essentially risk-free returns (over a long-enough period of time) that substantially outpace inflation? Or have we maybe been sold a bill of goods by the same financial industry/government policy machine that, just a few years ago, opportunistically looked at the historical data and told us with a straight face that housing prices would always go up?

posted by gd779 at 7:01 AM on May 12, 2013 [4 favorites]

What makes a stock a good investment? Since dividend payouts are now negligible (they weren't always), participants in the stock market, like participants in the housing market before them, rely on finding a "greater fool" to sell their stocks to at a profit. Historically, this has worked out well, for much the same reason that housing was a good investment for the Boomers: the combination of a demographic bulge, increases in productivity, and growing public acceptance of and participation in the market (driven, in the case of housing, in part by easily affordable mortgages provided to returning military members, and in the case of stocks, by IRA's and the decline of pensions) caused large, sustained price increases. But, as Herb Stein famously said, if something can't go on forever, it will stop. As the Boomers cash in their retirement accounts, and succeeding generations are both smaller and less able to invest (due to the economic recession, higher tax burdens, and the burden of paying for parents that have outlived their retirement savings), will there always be greater fools?

When you think about it, is it rational that unskilled consumers/investors should be able to sustainably generate essentially risk-free returns (over a long-enough period of time) that substantially outpace inflation? Or have we maybe been sold a bill of goods by the same financial industry/government policy machine that, just a few years ago, opportunistically looked at the historical data and told us with a straight face that housing prices would always go up?

posted by gd779 at 7:01 AM on May 12, 2013 [4 favorites]

Another factor to take into account when considering retirement investing is employer matching. If your employer matches 50 or 100% of your contribution up to a certain amount (many do), that suddenly makes investing in a 401k much more compelling than any other option.

posted by sophist at 7:02 AM on May 12, 2013 [1 favorite]

posted by sophist at 7:02 AM on May 12, 2013 [1 favorite]

Stock returns overtime reflect dividend payouts and growth in book value not just dividend returns. Payout and bv growth are functions of the return on equity. Overtime the return on equity equals the cost of equity which is a function of real rates and the perceived risk of investing equities.

The idea that only dividends represent real returns on equity is bogus. As is the idea that the premium equities earn above treasuries is some foible of history. The whole point is that it isn't some risk less premium. Equities are riskier. You can have massive drawdowns, you can't realistically invest in them of a time frame shorter than ten years. It isn't a free ride.

posted by JPD at 7:18 AM on May 12, 2013 [1 favorite]

The idea that only dividends represent real returns on equity is bogus. As is the idea that the premium equities earn above treasuries is some foible of history. The whole point is that it isn't some risk less premium. Equities are riskier. You can have massive drawdowns, you can't realistically invest in them of a time frame shorter than ten years. It isn't a free ride.

posted by JPD at 7:18 AM on May 12, 2013 [1 favorite]

Btw Credit Suisse publishes something called "global investment returns yearbook" that is a great resource for this sort of question.

posted by JPD at 7:22 AM on May 12, 2013

posted by JPD at 7:22 AM on May 12, 2013

Stock returns overtime reflect dividend payouts and growth in book value not just dividend returns.

Book value is an accounting fiction. How can I turn a profit based on the book value? Only by finding a greater fool. What if there aren't any (or aren't any that can afford to pay the price I want to charge)?

The idea that stockholders have a residual claim on the assets of the corporation is impractical, both because corporations never choose to dissolve their business and distribute their assets (moral hazard makes that impossible even if it is theoretically the right thing to do) but also because stocks generally trade at multiples of price to book value, representing a guaranteed loss. The premium over book value represents the speculative value of the greater fool.

posted by gd779 at 7:46 AM on May 12, 2013

Book value is an accounting fiction. How can I turn a profit based on the book value? Only by finding a greater fool. What if there aren't any (or aren't any that can afford to pay the price I want to charge)?

The idea that stockholders have a residual claim on the assets of the corporation is impractical, both because corporations never choose to dissolve their business and distribute their assets (moral hazard makes that impossible even if it is theoretically the right thing to do) but also because stocks generally trade at multiples of price to book value, representing a guaranteed loss. The premium over book value represents the speculative value of the greater fool.

posted by gd779 at 7:46 AM on May 12, 2013

Equities are riskier. You can have massive drawdowns, you can't realistically invest in them of a time frame shorter than ten years.

A lock-in period isn't the same as risk. The idea that we can magically make risk of loss vanish by holding stocks for long enough periods is sort of questionable, isn't it? Stocks are not subject to the laws of physics, and past performance is no guaranty of future results. If stocks really are risky, if there is no free ride, then there must be the real possibility of loss: not just in the short term, but in the long term as well. And a massive demographic shift coupled with a recession and the associated increased tax burdens might be just the thing to cause stocks to dip for a generation. But as Dennis Miller would say, that's just my opinion, I could be wrong.

posted by gd779 at 7:53 AM on May 12, 2013

A lock-in period isn't the same as risk. The idea that we can magically make risk of loss vanish by holding stocks for long enough periods is sort of questionable, isn't it? Stocks are not subject to the laws of physics, and past performance is no guaranty of future results. If stocks really are risky, if there is no free ride, then there must be the real possibility of loss: not just in the short term, but in the long term as well. And a massive demographic shift coupled with a recession and the associated increased tax burdens might be just the thing to cause stocks to dip for a generation. But as Dennis Miller would say, that's just my opinion, I could be wrong.

posted by gd779 at 7:53 AM on May 12, 2013

The stock market is risky, and you're quite right to worry about non market risks as well. You could save for 40 years "aaaaand it's gone".

Diversifying into real estate or other non public investments seems like a good idea, but it's not easy. I haven't done it and most won't.

In any case deliberately choosing a retirement of government cheese and cat food is a mistake. Adopting that attitude will likely have negative effects in the short/medium term. You can make a financial wreck of yourself long before retirement age. It's common, even. The people who do it don't enjoy it.

Don't expect 10% returns, but put something aside for retirement anyway.

posted by mattu at 9:06 AM on May 12, 2013

Diversifying into real estate or other non public investments seems like a good idea, but it's not easy. I haven't done it and most won't.

In any case deliberately choosing a retirement of government cheese and cat food is a mistake. Adopting that attitude will likely have negative effects in the short/medium term. You can make a financial wreck of yourself long before retirement age. It's common, even. The people who do it don't enjoy it.

Don't expect 10% returns, but put something aside for retirement anyway.

posted by mattu at 9:06 AM on May 12, 2013

Since dividend payouts are now negligible (they weren't always), participants in the stock market, like participants in the housing market before them, rely on finding a "greater fool" to sell their stocks to at a profit.

gd779, the first step in understanding why your concerns about the "financial industry/government policy machine" are misguided is to recognize the following.

You suggest that if a company never pays a dividend and never is liquidated, then any increases in the price of its shares must be purely speculative gains which do not represent an increase in real value.

That's just not correct. If I plant a seed, and grow ten seeds, and plant them all, and grow a hundred seeds, and plant them all, and grow a thousand seeds, and never actually eat any of the fruit, but rather reinvest each harvest into future growth -- do you really believe that I'm generating zero wealth, and that anyone who bought a share of my enterprise must be a greater fool? There's a genuine, and genuinely-growing, underlying value to my enterprise whether or not we actually get around to consuming the fruits of the growth.

stocks generally trade at multiples of price to book value, representing a guaranteed loss. The premium over book value represents the speculative value of the greater fool.

You're ignoring goodwill (the real value from the fact that consumers recognize a brand's reputation and consequently will buy its products with more confidence) and logistical value (the real value from the fact that the firm is a well-organized system with established channels for getting things done efficiently). Market cap is higher than book value because market cap can account for those values. (The fact that McDonald's is worth more in the form of a firm, than in the form of a warehouse full of deep fryers and employment contracts, is precisely why people don't go about liquidating successful firms. Real economic value, not just speculative value, would be lost if they did.)

Of course there are no guarantees in any investment, but the OP's question amounts to "will the average public company increase in value over time?" and your answer is "no, economic growth is an illusion." OP would not be well-served by taking that answer seriously.

posted by foursentences at 9:43 AM on May 12, 2013 [2 favorites]

gd779, the first step in understanding why your concerns about the "financial industry/government policy machine" are misguided is to recognize the following.

You suggest that if a company never pays a dividend and never is liquidated, then any increases in the price of its shares must be purely speculative gains which do not represent an increase in real value.

That's just not correct. If I plant a seed, and grow ten seeds, and plant them all, and grow a hundred seeds, and plant them all, and grow a thousand seeds, and never actually eat any of the fruit, but rather reinvest each harvest into future growth -- do you really believe that I'm generating zero wealth, and that anyone who bought a share of my enterprise must be a greater fool? There's a genuine, and genuinely-growing, underlying value to my enterprise whether or not we actually get around to consuming the fruits of the growth.

stocks generally trade at multiples of price to book value, representing a guaranteed loss. The premium over book value represents the speculative value of the greater fool.

You're ignoring goodwill (the real value from the fact that consumers recognize a brand's reputation and consequently will buy its products with more confidence) and logistical value (the real value from the fact that the firm is a well-organized system with established channels for getting things done efficiently). Market cap is higher than book value because market cap can account for those values. (The fact that McDonald's is worth more in the form of a firm, than in the form of a warehouse full of deep fryers and employment contracts, is precisely why people don't go about liquidating successful firms. Real economic value, not just speculative value, would be lost if they did.)

Of course there are no guarantees in any investment, but the OP's question amounts to "will the average public company increase in value over time?" and your answer is "no, economic growth is an illusion." OP would not be well-served by taking that answer seriously.

posted by foursentences at 9:43 AM on May 12, 2013 [2 favorites]

I really like this graphic for explaining stock returns vs time horizon. And I just realized the guy who originated it lives in town. I think the NYTimes did an excellent job cleaning up the original!

As to reading that chart, the colors represent critical thresholds: dark red fails to outpace inflation, light red loses to a bond portfolio, and grey represents the below average year returns, and greens represent above average returns. To answer the question of what returns look like, I first need to explain that there isn't such a thing as THE long term return. Rather, as your horizon expands, your risk terms get smaller. A diagonal at offset X will give you a series of returns from investing in stocks for X years. Visually, the further away your diagonal is from the edge, the less volatile the returns are. At 30 years, it's pretty squarely in the 3-7 range. No huge winners and no huge losers.

So yeah, I guess, followup question: If the returns really were just 2%, how could I feel more okay about retirement, and not that I'm throwing my money down a black hole?

Most goldbugs I know basically assume gold tracks inflation. That's not very true, but for the sake of argument, lets say the market returns are 2 percent post inflation, and gold is 0. Which number is bigger?

posted by pwnguin at 12:15 PM on May 12, 2013 [2 favorites]

As to reading that chart, the colors represent critical thresholds: dark red fails to outpace inflation, light red loses to a bond portfolio, and grey represents the below average year returns, and greens represent above average returns. To answer the question of what returns look like, I first need to explain that there isn't such a thing as THE long term return. Rather, as your horizon expands, your risk terms get smaller. A diagonal at offset X will give you a series of returns from investing in stocks for X years. Visually, the further away your diagonal is from the edge, the less volatile the returns are. At 30 years, it's pretty squarely in the 3-7 range. No huge winners and no huge losers.

So yeah, I guess, followup question: If the returns really were just 2%, how could I feel more okay about retirement, and not that I'm throwing my money down a black hole?

Most goldbugs I know basically assume gold tracks inflation. That's not very true, but for the sake of argument, lets say the market returns are 2 percent post inflation, and gold is 0. Which number is bigger?

posted by pwnguin at 12:15 PM on May 12, 2013 [2 favorites]

If I plant a seed, and grow ten seeds, and plant them all, and grow a hundred seeds, and plant them all, and grow a thousand seeds, and never actually eat any of the fruit, but rather reinvest each harvest into future growth -- do you really believe that I'm generating zero wealth, and that anyone who bought a share of my enterprise must be a greater fool? There's a genuine, and genuinely-growing, underlying value to my enterprise whether or not we actually get around to consuming the fruits of the growth.

That's a very astute analogy, foursentences. But here is the flaw: in your analogy, you are the owner of the seeds and the fruit. At some point you will, presumably, "cash in" your investment by selling and/or eating some of the fruit. But what if I offered to sell you, not an ownership interest in the farm, but a derivitave contract that could never be redeemed for fruit and/or a share of the profits, but could only be sold to another investor until the day that a drought wipes out the farm and all the crops and the contract becomes worthless? That is a better analogy for modern publicly traded stocks. Would that contract be a good investment?

posted by gd779 at 12:40 PM on May 12, 2013 [1 favorite]

That's a very astute analogy, foursentences. But here is the flaw: in your analogy, you are the owner of the seeds and the fruit. At some point you will, presumably, "cash in" your investment by selling and/or eating some of the fruit. But what if I offered to sell you, not an ownership interest in the farm, but a derivitave contract that could never be redeemed for fruit and/or a share of the profits, but could only be sold to another investor until the day that a drought wipes out the farm and all the crops and the contract becomes worthless? That is a better analogy for modern publicly traded stocks. Would that contract be a good investment?

posted by gd779 at 12:40 PM on May 12, 2013 [1 favorite]

pwnguin, I'd really like to thank you for those two reference graphs. They're going to take some time to digest!

posted by IAmBroom at 1:49 PM on May 12, 2013

posted by IAmBroom at 1:49 PM on May 12, 2013

I can cash in my fruit every day the stock exchange is open. If the business I fractionally own doesn't earn its cost of equity on its marginal investment of retained earnings eventually the market prices that in to the shares and it becomes in my interest or your interest or some corporate raiders interest or some strategic buyers interest to force out management and/or sell off the business piece meal.

Think about the math - If I get a dollar of dividends I have to reinvest that dollar somewhere - so I don't care if I make that reinvestment decision or the companies management makes that reinvestment decision, assuming that both of us are average decision makers

taxes aside (which favors retaining earnings BTW) paying out a dividend is the exact same thing to me as reinvesting retained earnings at the companies cost of equity. As long as they price that the same way I do, we should be ok. Often they do not, but that's why the marginal returns on businesses trend towards economic break even over time and why stocks should in equilibrium be worth their economic book value.

posted by JPD at 1:53 PM on May 12, 2013

Think about the math - If I get a dollar of dividends I have to reinvest that dollar somewhere - so I don't care if I make that reinvestment decision or the companies management makes that reinvestment decision, assuming that both of us are average decision makers

taxes aside (which favors retaining earnings BTW) paying out a dividend is the exact same thing to me as reinvesting retained earnings at the companies cost of equity. As long as they price that the same way I do, we should be ok. Often they do not, but that's why the marginal returns on businesses trend towards economic break even over time and why stocks should in equilibrium be worth their economic book value.

posted by JPD at 1:53 PM on May 12, 2013

I think you should also look at something else, which is volatility. Investing in gold is investing in one thing. Investing in a broadly diversified stock market index fund is investing in many things (companies, industries, etc.). If gold returns x% on average over 100 years and stocks return y% on average over 100 years, but you are investing for 5, 10, 15, 20, or 30 years, those figures are not illuminating the much higher volatility and risk of a single investment vs. a highly diversified investment.

posted by Dansaman at 3:57 PM on May 12, 2013

posted by Dansaman at 3:57 PM on May 12, 2013

This thread is closed to new comments.

posted by mygoditsbob at 5:51 AM on May 12, 2013