US healthcare for the young and temporarily of-no-fixed-abode?

May 11, 2023 5:09 AM Subscribe

A young relative (YR) of mine is about to graduate university, but does not yet have a job lined up. Simultaneously, coincidentally, and for reasons, their dual-citizen parents have left the US and returned to their native country. This leaves YR with no parental home to return to, and no remaining connection to their current state of residence. Thankfully, they do have a few other US relatives, spread across several other US states, and the plan is for YR to basically couch-surf among their homes until they can get a proper job (which may take some time). The question: what should YR do for health insurance in the meantime? Is the right move to repeatedly sign up for, and then cancel, exchange plans as they move around (sometimes potentially for just a couple weeks at a time?)? Is there such a thing as a state exchange plan that includes non-emergency out-of-state coverage?

Note: YR is generally healthy, but does have some ongoing health needs: emergency-only coverage wouldn't cut it. Also, YR is a US citizen. There's some budget available to make this work - but cheaper is better.

Note: YR is generally healthy, but does have some ongoing health needs: emergency-only coverage wouldn't cut it. Also, YR is a US citizen. There's some budget available to make this work - but cheaper is better.

Can YR time their moves around their medical needs at all? Like, if they have a monthly appointment or prescription for X, can they plan to always be in or near State Y at that time?

I'm assuming that if the relatives were close enough together that YR could easily commute to one central place for healthcare you would have mentioned that, and that telehealth is not an option for YR's ongoing health needs.

Another possibility would be to get whatever plan is cheapest and pay out-of-pocket when necessary, but the feasibility/affordability of that greatly depends on what kind of care YR needs.

Also, beyond the question of insurance, does YR have a plan for finding providers in all these different states? How is that going to work?

posted by mskyle at 6:00 AM on May 11, 2023

I'm assuming that if the relatives were close enough together that YR could easily commute to one central place for healthcare you would have mentioned that, and that telehealth is not an option for YR's ongoing health needs.

Another possibility would be to get whatever plan is cheapest and pay out-of-pocket when necessary, but the feasibility/affordability of that greatly depends on what kind of care YR needs.

Also, beyond the question of insurance, does YR have a plan for finding providers in all these different states? How is that going to work?

posted by mskyle at 6:00 AM on May 11, 2023

I think the most straightforward answer is that YR needs to identify the best state with regards to a willing long-term host and proximity to the necessary medical care, and make that their base of operations and insurance state. The other relatives can provide some financial support in lieu of a couch, if this would be a burden on the host.

They can go visit the other relatives briefly as part of a job-application flurry (apply to a number of jobs in that area remotely, line up in-person interviews for a specific week in which they don't need medical appointments, travel there and go to them). And also to give Primary Host a bit of a break. It's not unusual for recent grads (or about-to-grads) to apply for jobs in places other than their current residence, and should require no more detailed explanation than "I do already have somewhere to live in YourCity if that's where I find a job."

posted by Lyn Never at 6:21 AM on May 11, 2023 [5 favorites]

They can go visit the other relatives briefly as part of a job-application flurry (apply to a number of jobs in that area remotely, line up in-person interviews for a specific week in which they don't need medical appointments, travel there and go to them). And also to give Primary Host a bit of a break. It's not unusual for recent grads (or about-to-grads) to apply for jobs in places other than their current residence, and should require no more detailed explanation than "I do already have somewhere to live in YourCity if that's where I find a job."

posted by Lyn Never at 6:21 AM on May 11, 2023 [5 favorites]

In some states they will likely qualify for Medicaid. Figure out which relative is in a state with the best benefits and get them there. Rely on telehealth as much as possible.

posted by metasarah at 7:14 AM on May 11, 2023 [1 favorite]

posted by metasarah at 7:14 AM on May 11, 2023 [1 favorite]

The university/college may have a student policy in place that YR could get into or if they're already on it, it may go out some months after graduation.

Did the parents move to a country in this hemisphere that's known for cheap reliable healthcare? If so, that may be the solution.

posted by fiercekitten at 7:43 AM on May 11, 2023 [1 favorite]

Did the parents move to a country in this hemisphere that's known for cheap reliable healthcare? If so, that may be the solution.

posted by fiercekitten at 7:43 AM on May 11, 2023 [1 favorite]

When I was in a similar situation I got a PPO plan which would in theory have more generous coverage for “out of network” providers.

An idea though - what do RVers and van life folks who are on the road for months at a time do for health insurance?

posted by forkisbetter at 5:00 PM on May 11, 2023

An idea though - what do RVers and van life folks who are on the road for months at a time do for health insurance?

posted by forkisbetter at 5:00 PM on May 11, 2023

Does he/she have regular doctors? Maybe it would be worth talking to a patient financial advocate for the doctors' group/hospital to see if they could be of help. .

posted by greatalleycat at 6:27 PM on May 11, 2023

posted by greatalleycat at 6:27 PM on May 11, 2023

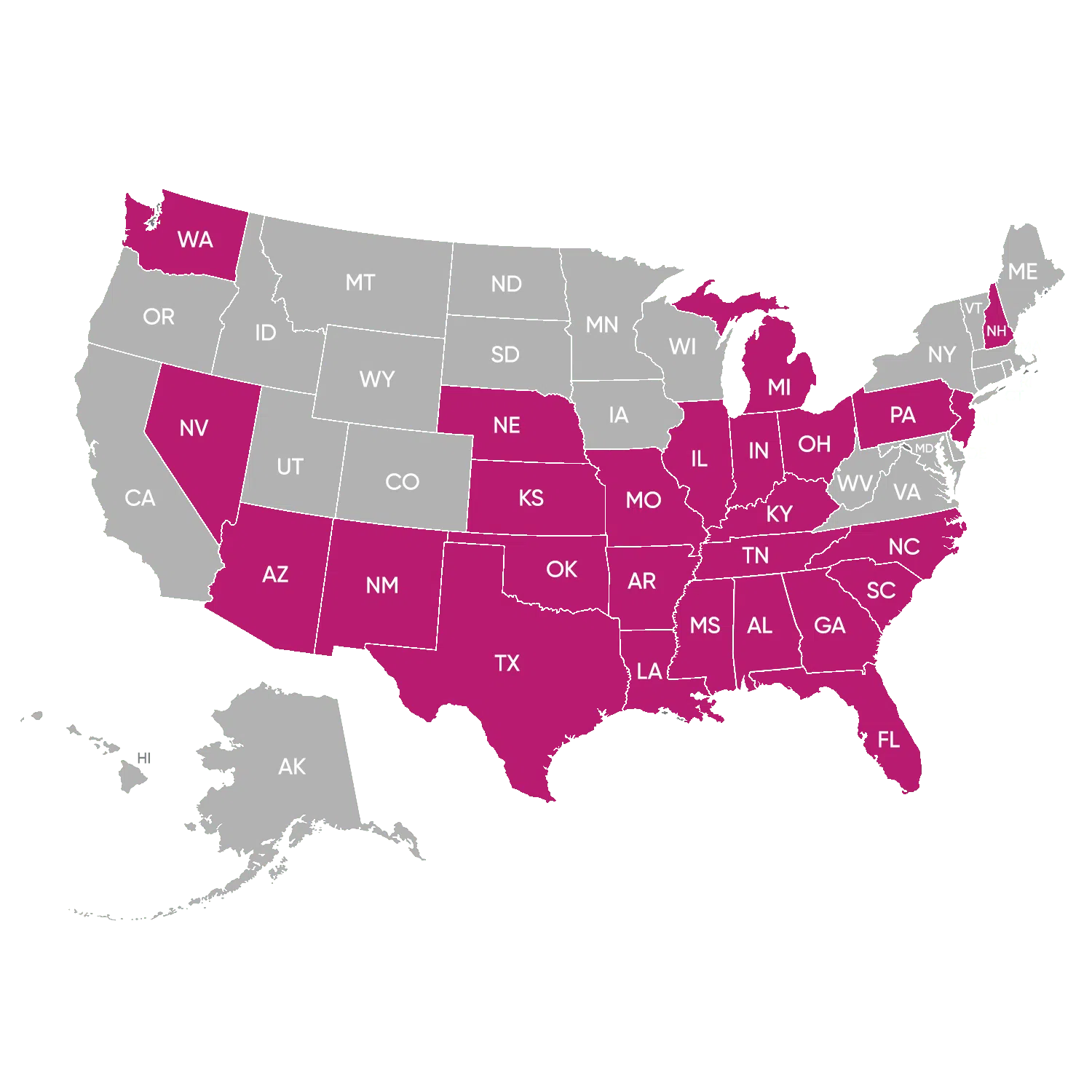

FWIW I have a exchange health insurance through Ambetter/Home State Health. They have coverage in all these states.

Over the past few years I spent a considerable amount of time each year living with my parents in a different state. As far as I understand, if I lived in one of the states where Ambetter has coverage, it would have been no problem at all. I could just access care from one of the physicians, clinics, hospitals, etc, that is in their plan, whichever state that might be, and it would be all the same.

However - my parents state, by bad luck, is not one of their covered states. This was a pretty considerable pain in the #$$. What I did:

- I considered traveling to an adjoining state where they do have coverage, or returning to my home state, when I needed any substantial care. I never had to do that but it was an option.

- I was able to have telehealth appointments with my established doctors back home on a few occasions. There are restrictions in where doctors located/licensed in state X can provide care to patients in state Y, however. During Covid some of that was loosened, though I believe it is tightened up again to a degree. HOWEVER, to a large degree I just didn't tell the doctor where I was. It was my regular doctor whose office is just down the street from my house, so from my point of view whether I am teleconferencing in from just down the block or wherever I happen to be at the moment, it's all the same to me and I just don't mention it one way or the other.

- I used the plan's telehealth benefit quite a few times. This worked well. This is what I used for the equivalent of urgent care visits - my ear hurts, what should I do, I think I might have covid or the flu, what should I do, etc. They could write me a prescription, order needed tests, etc etc. See below for how I got prescriptions filled and lab work down while out of state.

- For my plan, it turned out that 'emergency care' meant literally that - an emergency room visit and (presumably) the ensuing hospital admission, until transportation back home can be arranged, if that happens. That is fine and dandy, but for example it DID NOT cover urgent care visits. Read your coverage details CAREFULLY because some might cover this and some not. I ASSUMED that "emergency" coverage would include something like, I'm visiting out of state and come down with a flu or covid and need to visit urgent care. But no. Only if you visit the actual ER (probably more expensive, even WITH insurance), not the plain old cheaper Urgent Care. (I do think many/most plans will cover urgent care - but worth checking and probably a giant pain in the #$$ to get reimbursed if this should happen to you.

- To a degree you can just pay out of pocket for a couple of urgent care visits out of state. Depending on your plan, deductible, etc you are probably going to be paying for a few such expenses throughout the year regardless of what state you are in, so you could just budget in say 4 urgent care visits a year into your health care budget for the year.

- For lab work, I was able to use a national chain like LabCorp, which accepted my insurance even though the insurance was based in another state. So for example in one instance, I had a telehealth visit with my regular family doctor back home, he wanted labs, I asked him to sent the lab request to LabCorp, I went to LabCorp in the state where I was visiting, and got the lab work done no problem.

Similarly, I transferred all my prescriptions to Walmart before leaving, then had Walmart transfer them to a local store in the area I was staying. Being a national chain, they had an agreement with Ambetter and I didn't matter what state I was in or what store the actual prescription came from. The same would work for CVS, Walgreens, and similar chains, or whatever mail order pharmacy your plan might offer. Then later I switched all my drugs to CostPlus Drugs, which doesn't deal with insurance but somehow manages to keep all drug prices (for the ones I take, and the ones they offer - they don't carry everything) lower even with no insurance than what I usually pay for drugs covered by insurance.

- I thought about changing plans to the one in my current state. This is possible because moving to a new state is a qualifying event for marketplace coverage. But the major problem is, you start right over again with deductible, out of pocket maximum, etc etc etc when you switch to a new plan. So if you switched to a new plan in a new state say 4X per year you would basically have no coverage at all for practical purposes. I guess it would cover something truly catastrophically expensive, but for day-to-day and planned type medical expenses, that's going to do nothing whatsoever.

General tips:

- Look for health plans on your exchange that have coverage in many states (most do), and see if you can find one that covers all the states you are planning to be in. Then ALSO call them up and make sure if you purchase from the exchange in State X the plan will also be valid for State Y. (I did ask the Ambetter folks about this and said it was OK. This might be different for different insurance companies, however.)

- One advantage here is the person can somewhat choose their state of residence - in case the most desirable plan is available in one state only, just move there first, purchase the plan, and proceed. (I am not sure what exact legal requirements are needed to establish residence, but for something like this it is usually just that you are living there, have an address of residence, and are planning to make this your main residence. That doesn't prohibit you from leaving the state to visit other places - if you consider X your main residence and are planning to return there that is about all you need. Probably. My point is, your person should pick one place that will be considered the main residence and indicate that on all paperwork etc. From then on, consider that place the "main residence" and everywhere else is a "temporary visit".)

- It might worth talking with someone like an insurance broker or one of those groups that offer help in applying for insurance on the exchange. They might know what companies or plans to look at in your situation.

- On the Exchange, trying to find an insurance plan that has both decent coverage and also covers the exact states you are interested in might be something of a giant pain in the #$$.

- Healthcare.gov has a page on how moving affects your coverage. Once again, I would NOT consider every time I am couch surfing for a different relative for 3 weeks a "new residence". Just choose one residence and count that as your permanent residence until you actually move permanently to somewhere else (ie, rent your own apartment, buy a house or whatever).

- Some people will purchase something like catastrophic insurance in situations like this. The idea is, you just figure out your typical annual health care costs and plan a budget to pay for them. Many times this is less than the cost of doing the same with insurance - once you factor in the monthly insurance premiums. But then you also purchase the catastrophic insurance, which gives you coverage in case you a hit by a semi-truck or have some other relatively rare but catastrophic event happen. It is maybe not the best option, but it is an option to consider. Also, this would be easier to transfer state to state in case that is needed - because you won't generally have any deductible or out-of-pocket-max amounts to consider. Just don't forget to budget & save for your regular/expected health care costs.

TL;DR: What a giant dysfunctional pain in the #$$ our entire health care system is.

Good luck!

posted by flug at 2:16 PM on May 12, 2023

{kind=link}

Over the past few years I spent a considerable amount of time each year living with my parents in a different state. As far as I understand, if I lived in one of the states where Ambetter has coverage, it would have been no problem at all. I could just access care from one of the physicians, clinics, hospitals, etc, that is in their plan, whichever state that might be, and it would be all the same.

However - my parents state, by bad luck, is not one of their covered states. This was a pretty considerable pain in the #$$. What I did:

- I considered traveling to an adjoining state where they do have coverage, or returning to my home state, when I needed any substantial care. I never had to do that but it was an option.

- I was able to have telehealth appointments with my established doctors back home on a few occasions. There are restrictions in where doctors located/licensed in state X can provide care to patients in state Y, however. During Covid some of that was loosened, though I believe it is tightened up again to a degree. HOWEVER, to a large degree I just didn't tell the doctor where I was. It was my regular doctor whose office is just down the street from my house, so from my point of view whether I am teleconferencing in from just down the block or wherever I happen to be at the moment, it's all the same to me and I just don't mention it one way or the other.

- I used the plan's telehealth benefit quite a few times. This worked well. This is what I used for the equivalent of urgent care visits - my ear hurts, what should I do, I think I might have covid or the flu, what should I do, etc. They could write me a prescription, order needed tests, etc etc. See below for how I got prescriptions filled and lab work down while out of state.

- For my plan, it turned out that 'emergency care' meant literally that - an emergency room visit and (presumably) the ensuing hospital admission, until transportation back home can be arranged, if that happens. That is fine and dandy, but for example it DID NOT cover urgent care visits. Read your coverage details CAREFULLY because some might cover this and some not. I ASSUMED that "emergency" coverage would include something like, I'm visiting out of state and come down with a flu or covid and need to visit urgent care. But no. Only if you visit the actual ER (probably more expensive, even WITH insurance), not the plain old cheaper Urgent Care. (I do think many/most plans will cover urgent care - but worth checking and probably a giant pain in the #$$ to get reimbursed if this should happen to you.

- To a degree you can just pay out of pocket for a couple of urgent care visits out of state. Depending on your plan, deductible, etc you are probably going to be paying for a few such expenses throughout the year regardless of what state you are in, so you could just budget in say 4 urgent care visits a year into your health care budget for the year.

- For lab work, I was able to use a national chain like LabCorp, which accepted my insurance even though the insurance was based in another state. So for example in one instance, I had a telehealth visit with my regular family doctor back home, he wanted labs, I asked him to sent the lab request to LabCorp, I went to LabCorp in the state where I was visiting, and got the lab work done no problem.

Similarly, I transferred all my prescriptions to Walmart before leaving, then had Walmart transfer them to a local store in the area I was staying. Being a national chain, they had an agreement with Ambetter and I didn't matter what state I was in or what store the actual prescription came from. The same would work for CVS, Walgreens, and similar chains, or whatever mail order pharmacy your plan might offer. Then later I switched all my drugs to CostPlus Drugs, which doesn't deal with insurance but somehow manages to keep all drug prices (for the ones I take, and the ones they offer - they don't carry everything) lower even with no insurance than what I usually pay for drugs covered by insurance.

- I thought about changing plans to the one in my current state. This is possible because moving to a new state is a qualifying event for marketplace coverage. But the major problem is, you start right over again with deductible, out of pocket maximum, etc etc etc when you switch to a new plan. So if you switched to a new plan in a new state say 4X per year you would basically have no coverage at all for practical purposes. I guess it would cover something truly catastrophically expensive, but for day-to-day and planned type medical expenses, that's going to do nothing whatsoever.

General tips:

- Look for health plans on your exchange that have coverage in many states (most do), and see if you can find one that covers all the states you are planning to be in. Then ALSO call them up and make sure if you purchase from the exchange in State X the plan will also be valid for State Y. (I did ask the Ambetter folks about this and said it was OK. This might be different for different insurance companies, however.)

- One advantage here is the person can somewhat choose their state of residence - in case the most desirable plan is available in one state only, just move there first, purchase the plan, and proceed. (I am not sure what exact legal requirements are needed to establish residence, but for something like this it is usually just that you are living there, have an address of residence, and are planning to make this your main residence. That doesn't prohibit you from leaving the state to visit other places - if you consider X your main residence and are planning to return there that is about all you need. Probably. My point is, your person should pick one place that will be considered the main residence and indicate that on all paperwork etc. From then on, consider that place the "main residence" and everywhere else is a "temporary visit".)

- It might worth talking with someone like an insurance broker or one of those groups that offer help in applying for insurance on the exchange. They might know what companies or plans to look at in your situation.

- On the Exchange, trying to find an insurance plan that has both decent coverage and also covers the exact states you are interested in might be something of a giant pain in the #$$.

- Healthcare.gov has a page on how moving affects your coverage. Once again, I would NOT consider every time I am couch surfing for a different relative for 3 weeks a "new residence". Just choose one residence and count that as your permanent residence until you actually move permanently to somewhere else (ie, rent your own apartment, buy a house or whatever).

- Some people will purchase something like catastrophic insurance in situations like this. The idea is, you just figure out your typical annual health care costs and plan a budget to pay for them. Many times this is less than the cost of doing the same with insurance - once you factor in the monthly insurance premiums. But then you also purchase the catastrophic insurance, which gives you coverage in case you a hit by a semi-truck or have some other relatively rare but catastrophic event happen. It is maybe not the best option, but it is an option to consider. Also, this would be easier to transfer state to state in case that is needed - because you won't generally have any deductible or out-of-pocket-max amounts to consider. Just don't forget to budget & save for your regular/expected health care costs.

TL;DR: What a giant dysfunctional pain in the #$$ our entire health care system is.

Good luck!

posted by flug at 2:16 PM on May 12, 2023

This article covers health insurance options for itinerant people, and mentions that Florida is the only state whose health care exchange plans offer nationwide coverage. It might be worth checking out of that is actually the case, and then establishing residence in Florida if that is an option.

posted by flug at 2:25 PM on May 12, 2023

posted by flug at 2:25 PM on May 12, 2023

You are not logged in, either login or create an account to post comments

posted by hoyland at 5:47 AM on May 11, 2023